Everybody’s angry. Whether it’s the latest round of tariffs, the rising national debt, or the Bezos wedding, the news and social media are filled with outrage. I’m not active on social media, but I’ve heard stories.

If we’re into politics, there are unlimited stories on both left and right leaning media sites to get our dander up. And then we have the Justin Baldoni/Blake Lively scandal. Talk about distraction!

Distraction

We work hard. Our lives can be stressful at times. It’s nice to have a distraction.

Unfortunately, our involvement with these distractions can make us take our eye off the ball. All of a sudden, we’re wrapped up and we lose focus on things that matter.

I think this is why some politicians are so successful. They’re like a magician. The get us distracted looking at the shiny object and next thing we know they have our wallet. But that’s a story for another day.

I’m Angry

Why am I angry today?

I’m not pissed. It’s a beautiful summer day. I spent yesterday with my 9 month old granddaughter, and maybe some golf later today. Why be angry?

But…

I recently got a notice that my auto, home and umbrella insurance policies were renewing. For most people this is a non-event. We’re set up for auto-pay and auto-renewal. We all hate insurance and insurance companies. Insurance is expensive and there’s no alternative so we just let it happen.

Don’t.

Before my auto-pay kicks in, I updated my insurance spreadsheet (Yes, of course I have an insurance spreadsheet. Don’t you?)

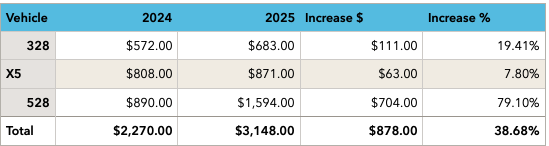

Here’s a peek.

Forget the price of eggs, the increases in insurance costs are ridiculous. My cost was up 26% last year and another 23% this year.

Vito Corleone would be proud.

Let’s take a deeper dive.

My wife and I have 3 vehicles. One is up 7.8%. I can live with that, but why is one up 79%???

Yup, I’m angry.

Why?

I have an insurance agent. This is relatively new for me. I always believed that I would get a better price going direct to a company like Progressive or GEICO, and this is what I had done for years.

A few years back, I decided I’d try an insurance agent. Just for fun, to see if the could beat my current rate.

I bet you’re thinking – yeah, that sounds like fun. I need to get out more. Have you heard that latest from Justin Baldoni???

Anyway, the first agent wouldn’t return calls and after chasing for a week, I gave up. The second one was amazing. She was really hustling to get info from me to find the best policy.

She ended up finding home, auto and umbrella insurance at $1,000 per year less than GEICO. Nice!!

And then it went up in 2023, and again in 2024, and here we are in 2025.

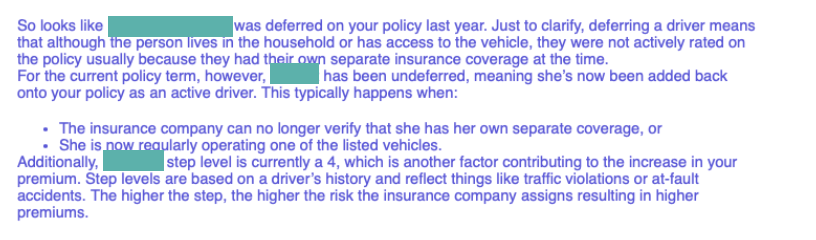

I asked about the huge 79% increase. Here’s what my insurance company told her.

Bravo for my insurance agent.

That’s Crap

So, my wife does not have an additional policy. We would know.

She had a minor accident last year and our auto insurance paid so it makes no sense that she was deferred, whatever that really means.

And she is the owner and primary driver of the 2 vehicles that did not go up in price (as much). It was the vehicle registered to me, on which I am listed as the primary driver, that went up 79%.

So why did my vehicle’s rate go up 79%?

I’m guessing someone has a boat payment coming due.

There’s no good answer. My insurance company would like more money and they’re relying on auto-pay, auto-renewal and the distractions of daily life to facilitate this transaction.

Wrap Up

So yes, I’m angry.

I was mad last year but the explanation then was more reasonable. This year’s story makes no sense.

I’ve asked my agent to start shopping for a new insurance provider.

For those who are regular readers (Hi Mike, Mike, Tony and Randy) you know that insurance shopping is an annual event in my house. Every year, usually in January, I shop for a better rate. Almost every year, I find one. I often save between $500 and $1,000 per year on insurance just by switching.

Part of the reason for this is that our insurance company relies on our blind loyalty and the gift (to them) of auto-renewal and auto-pay. Get a 10% policy rebate when signing up for auto-pay. We’ll increase your rate by 79%, but we’ll kindly give you 10% of that back.

And maybe even another 10% as a loyal customer discount. The discounts add up quick. While we’re watching that hand, they’re picking our pocket with the other.

Don’t take your eye off the ball.

I love to automate my payments and I love making my life simpler. Spending less time on paying my insurance bill is a win for me.

But be skeptical. Is my price going up? Is it going up inline with local averages? Does it make sense?

If not, it’s time to start shopping.

Trust but verify.

Yes, I’m angry. My insurance company is trying to fool me into paying more money than I should. There are lots of companies that would like my business. I’ll shop.

More updates when I find a new policy.

Agree 100% and wish I could shop our coverages around, I’ve tried numerous times (and with rentals – home & cars it’s over $10k total), yet no one even replies to the RFP to move it, so we are stuck !