While some of us invest in individual stocks and bonds, most regular folks invest our capital in various types of mutual funds and ETFs. But recently, individuals have been given the opportunity to invest in more exotic vehicles like private equity and private credit.

Today we’ll talk about what these are, and some of the benefits and risks so we can make informed decisions as to whether they make sense for us.

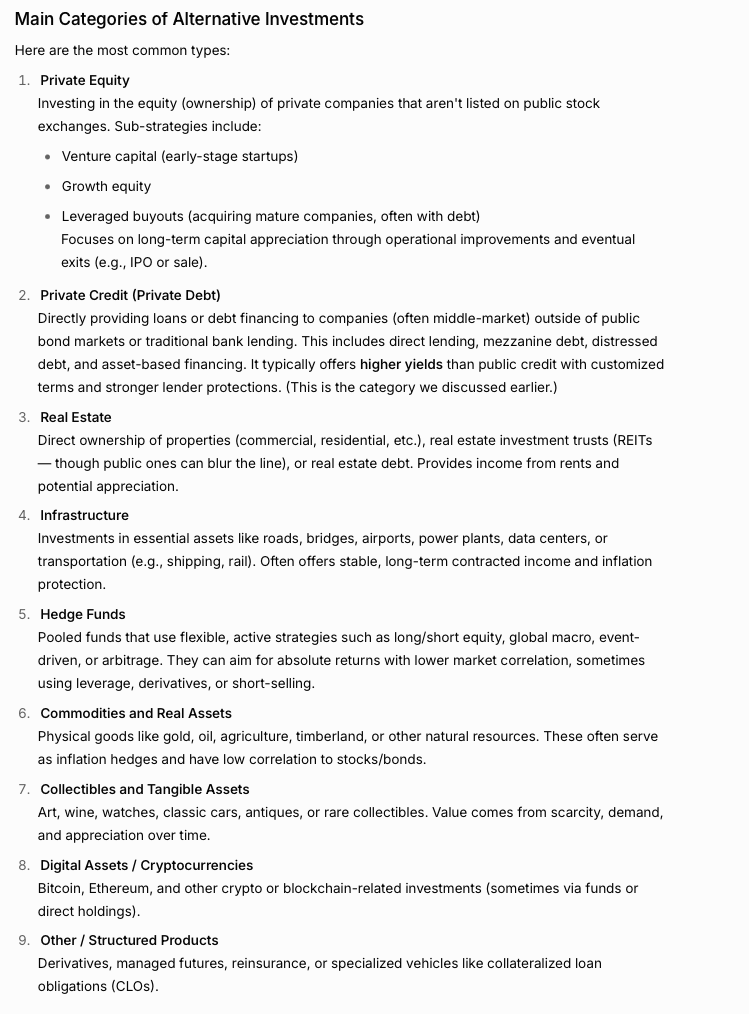

Alternative Investments

While private credit and private equity have gotten the headlines recently, they are part of a group of investments known as alternative investments (or Alts as the cool kids say).

Traditional investments are stocks, bonds, mutual funds, ETFs and Cash products. Alts covers the less-traditional forms of investments that are typically not available to the average Joe.

Here are some of the main categories of Alts from our friend Grok:

Why Do We Want It?

If you’ve ever seen the movie Super Pumped, you’re familiar with venture capital. The movie is a very entertaining look at the start of Uber. Kyle Chandler plays a venture capitalist whose firm is one of several financing Uber’s early days.

A venture capital firm is a bunch of rich folks who pool their money together and buy stuff.

And there are lots of smart folks out there with great ideas for businesses who need funding.

So the folks with the great ideas are out hunting for venture capital firms that would be willing to take a risk on their idea.

And for every Uber or Facebook that makes it big, there are many companies that fail. The beauty is that one winner can more than make up for dozens of failures.

Average Joes like us watch Super Pumped or the We Work story WeCrashed, and we want in on these moon-shot investments.

And none of us is making a huge windfall overnight by investing in a mutual fund. But if we could become an early investor in the next big thing…

We want it for the potential windfall. Fund our retirement overnight,

Private Equity

A lot of private equity is the venture capital world – providing capital to start-ups in the hopes that they’ll grow.

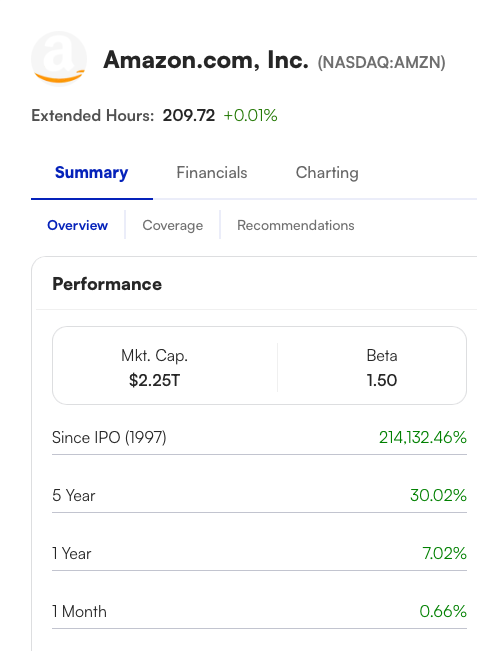

Take Amazon as an example. It is up an amazing amount since its IPO in 1997. Take a look.

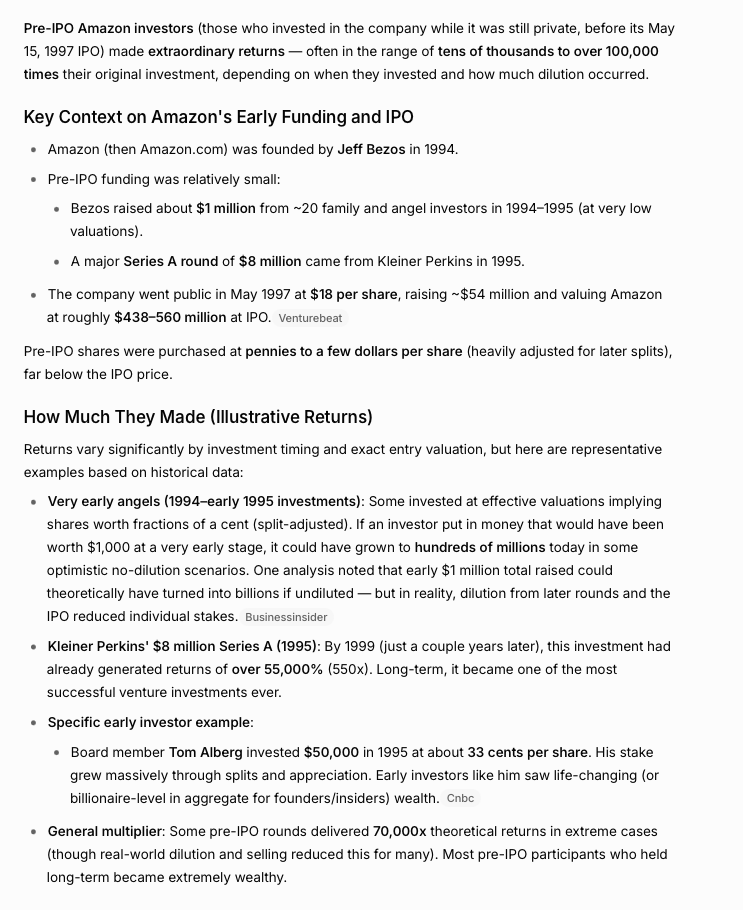

But imagine the growth if you got in on the ground floor – years before the IPO. Let’s ask Grok about it.

The good folks at Kleiner Perkins made 550 times their original investment in just 2 years. Imagine if I had $1,000 and the opportunity to invest. I would have had $550,000 in 2 years.

And then if I held on for 27 more…I can’t even calculate what that would be worth today…

Private Credit

Companies are borrowing money left and right.

A developer up the street from me is building apartments and there is a sign in front saying the project is financed by UniBank. The developer needs to buy materials and hire workers. That’s a huge expense so he borrows from his local bank.

Walmart is putting up a new SuperCenter in town. Actually, they’re putting up lots of SuperCenters around the globe. These ain’t cheap. Walmart will issue a bond and since it is a solid, dependable company, investors will line up to buy Walmart bonds.

UniBank will make a few percentage points on its loan to the developer and you and I can make about 4% per year if we buy the Walmart bond.

But, imagine if we could tap into the alternative bond markets. These are companies or groups that need financing that can’t secure it through traditional channels. We could make much higher returns.

Risk

It’s pretty apparent that the risk here is higher than we’d see in traditional investments.

Whether we’re getting in on the ground floor of a new business or we’re lending capital to a business with an unproven track record of repayment, the reward could be high. But the risk is also high.

We could invest in a company or 2 or 10 that go bust. We could loan money to someone who can’t pay it back.

Liquidity

I love ETFs.

I have some money invested in the iShares Core S&P 500 ETF (IVV). If I need to raise some cash, I can sell shares in my brokerage account and the trade processes immediately and I can spend the cash right away.

I’m now frustrated with my mutual funds. I put in a sell order today and it processes overnight. I don’t get the cash til tomorrow. Can you imagine??

That’s liquidity. I can trade assets for cash. Quickly.

Have you ever tried to sell a home or a car? In a seller’s market, you may be able to get this done in a few days or weeks, but in a buyer’s market, it could take much longer.

Homes, cars, baseball cards and other property are illiquid assets. We need to find a buyer and that can take time.

Let’s say I gave Jeff Bezos $1,000 in 1995 to help build Amazon. I would own a small piece of the book store operating out of Jeff’s garage.

Then I find that I need my $1,000.

I start running up and down the street asking anyone I see to buy my share of Amazon for $1,000. Amazon doesn’t trade on an exchange (yet), it’s private. I need to find a buyer. Most folks hadn’t even heard of Amazon and even if they had, who would want to buy?

We’ve become accustomed to traditional investments like stocks, bonds, mutual funds and ETFs that are liquid. We can get our money back within 24 hours or less.

Not so with alternative investments.

Real Estate

Real Estate is a popular form of private equity and provides a real-world example of why liquidity can be a problem.

Let’s say you, me and a few of our buddies start a real estate investment fund. We all put in some money and we go out and buy some properties. We hold aside some of the cash because we know we’ll have expenses. We may also keep a few dollars on the sideline for redemptions.

So we know that one of us may need to redeem some of our shares at some point. We can’t keep all of our cash on the sidelines or we couldn’t buy any property so we have to balance what we put towards property and what we hold for expenses and redemptions. Whatever is not invested won’t earn anything so we’re careful about minimizing this amount.

We go out and buy a few properties and then unexpectedly, 2 of us need to sell shares to pay for unexpected expenses. We don’t have enough cash on hand in the fund.

We have 2 choices.

- We can sell a property – this is not ideal because on a quick turn-around, we may lose money on the sale and we’ll definitely lose money on the buying and selling expenses

- We can limit redemptions

Selling properties is a sure way to go bankrupt fast.

So most alternative investments limit redemptions in some way. This allows them to keep a large portion of the investment capital invested and earning a return. They keep minimal cash on the sidelines for expenses and investor redemptions.

But if lots of investors want their money back, the fund may find itself in a position where it needs to sell assets at a loss and pay selling expenses. This is hugely detrimental to the fund and to other investors.

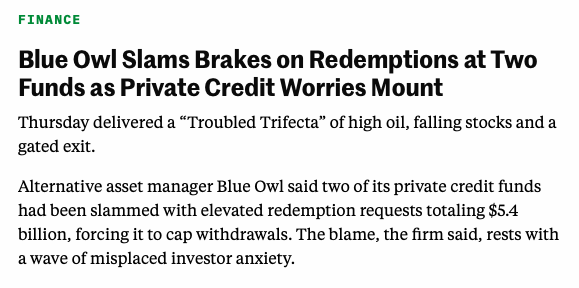

It Happens

Blue Owl Capital was in the news today for this very reason.

Suitability

Another big word.

Is this investment right for the customer?

That’s the meaning.

In the mutual fund advisory business, a lot of time is spent on suitability. Advisors who are fiduciaries, need to act in the best interests of customers. They need to recommend investments that have reasonable risks, reasonable expenses and are liquid.

Most mutual funds and ETFs fit the criteria because they are designed for the average investor.

Alternative investments may not be. Alternative investments are designed for accredited investors. These are investors who sign an agreement that they have a certain (high) level of assets and they have expertise in investment products.

These are the type of folks that have lots of other investments and lots of cash on hand and are less likely to ask for their money back. They’ll also understand how redemptions work and they’ll expect that they may not be able to get their money back even if they ask nicely.

Wrap Up

Venture capital is a popular field.

How cool would it be to get in on the ground floor of the next Uber or Amazon? We could make a killing.

But what would we do if many or even all of our investments didn’t pan out? And even if some did, they may take years to become profitable. What would we do?

And do we have enough cash on the sidelines ourselves to be able to lock money up in an investment for years?

Alternative investments can be lucrative, but they come with complexity and risk that most traditional investments don’t have.

It’s up to us to make sure we understand what we’re buying and how they operate before we commit our capital.