Prices are high.

No kidding!

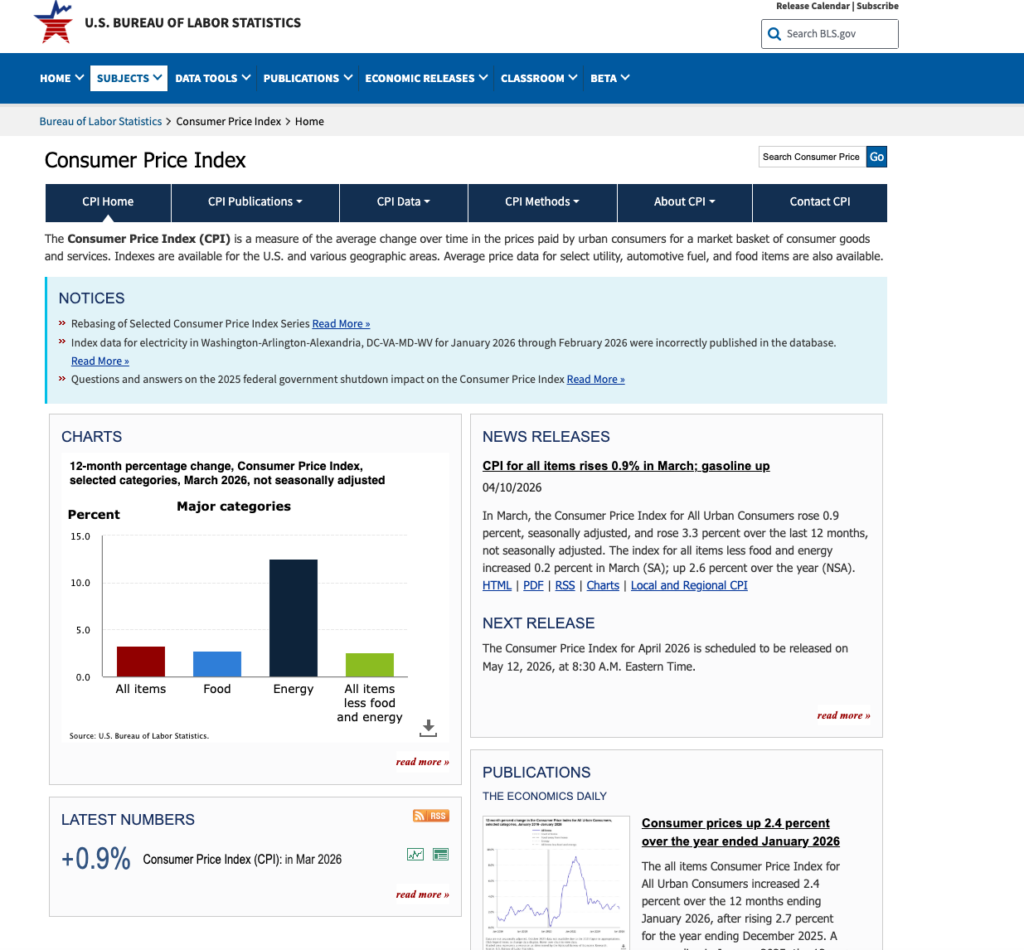

According to our friends at the Bureau of Labor Statistics, Inflation is up 3.3% over the last 12 months. Well above the target of 2%.

That said, I take everything that comes from the government with a large grain of salt, and especially from the BLS which has been gutted by layoffs.

But, this is what we’ve got, so let’s make the best of it.

And I think they’re right. It sure feels like inflation is up. Try buying beef. Or filling up the tank.

oil Prices are Up

Last year, in my energy basket, I bought a group of stocks in the energy and utilities sectors. Read more here and here. One company in the basket is Conoco Phillips, a large US oil and gas exploration and production company.

Conoco Phillips is up 19% since I bought it in 2025. It is up the most of all the companies in this basket.

This shouldn’t be surprising since we’ve all seen the prices at the pump skyrocket ever since the war in the middle east began. Everyday we see a new report about crude oil prices going up, and that makes a company that produces crude oil a winner.

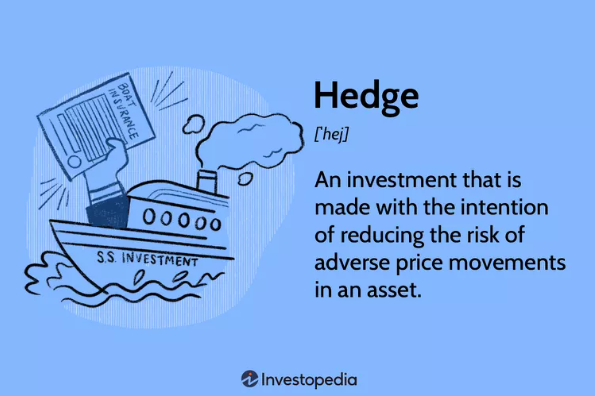

What is Hedging and How would i use it?

Investing in a company like Conoco Phillips can be a hedge against escalating oil prices.

My wallet is a little lighter because of the $4.59 per gallon I paid at the pump. And don’t even mention the $5.39 per gallon I paid for my last home heating oil fill-up.

But, I can offset that with the $2,330 gain in my Conoco Phillips shares. If I need to shore-up my budget, I could sell a few shares, take a profit and hold onto the rest for future hedging.

Airline companies do this. They use so much fuel that they can’t allow their businesses to be impacted when fuel prices soar. These companies buy oil futures when prices are relatively low to offset the cost when prices rise.

While I’m not suggesting any of us get into futures trading – this is a high risk game – I’ve always looked at my oil company investments as hedges against oil inflation.

And there is no magic to this. On 8/25/2025, I had no idea that the Iran war was coming or that oil prices would spike.

My share purchase was based on a general sense that the energy industry as a whole was attractive. Conoco Phillips being a fuel price hedge was just icing on the cake.

Happy Coincidence

Nothing happy about the war, but I was lucky in the timing of this trade. That doesn’t always happen. I held Devon Energy for years and eventually sold it for a loss. Devon is up 22% this year.

But that’s the way a hedge works. It’s almost like buying insurance. We pay for something we hope we’ll never have to use but if we need it it’s there.

Now that’s not entirely true. Oil spike or not, I felt Conoco Philllips would thrive in the next 5-10 years due to increased energy demand across the globe. I invested because of this. The oil price hedge is a nice added benefit.

Good Hedging and Bad Hedging – Choosing when to hedge

Health care is a cost that’s bleeding me dry. As a retiree who has not yet turned 65 and is not eligible for medicare, I’m spending $2,000 per month on private health care.

I’ve thought about a hedge for this. Why not invest in health care? Buy shares of United Health or a nice index ETF like the Fidelity MSCI Health Care Index ETF (FHLC).

I thought of this, however, I couldn’t come up with strong enough reasons why healthcare would beat the overall market and on top of that, I feel like healthcare companies are screwing us anyway so I don’t think I’d feel good about owning shares of one. I’d rather own Snap-On Tools, O’Reilly Automotive, Amazon or Netflix.

Using an S&P 500 investment as a hedge against rising prices

Another way to think about this is there are a lot of unexpected expenses we’d like to protect ourselves from. Is it really practical to hedge all of them? And what if they never happen?

The S&P 500 has proven to be a nice hedge. It’s made up of the 500 largest publicly traded US companies. It includes Conoco Phillips (and ExxonMobil and Chevron and some other oil and gas companies), Snap-On, O’Reilly, United Health, Amazon, Netflix and many others across all different sectors of the US economy.

Buying a few shares of a nice low cost S&P 500 fund can help hedge against cost increases.

While there is no guarantee that the S&P 500 will increase when prices increase, it has a solid track record of making money for investors.

Backtesting Some hedging strategies

I retired at the end of 2019.

Let’s say I wanted to hedge against higher prices so I take $10,000 and put it in a nice low-cost S&P 500 ETF like the iShares Core S&P 500 ETF (IVV)

My money in IVV would have more than doubled. I could sell half, take some profits to help pay expenses and keep $10,000 invested for future growth.

For comparison we can see that our other hedges didn’t work out as well. Though they still beat cash tucked under the mattress by a wide margin.

A Hedge is Not a Guarantee

Here’s what Investopedia has to say about a hedge,

The Conoco Phillips example is a true hedge. We’re buying an asset in the oil sector to insulate us from oil price increases. If oil prices go up, we’ll pay more at the pump, but our investment will likely increase in value to offset these costs.

In the S&P 500 example, we’re more loosely making an investment with the expectation that gains in that investment will offset future cost increases in our overall budget.

And either way, there is no guarantee that our hedge will work.

Let’s take a look at what would have happened if I had applied the S&P 500 hedge strategy when I was laid off from my job in 2008.

I was out of work on 10/20/2008. Let’s say I bought $10,000 of IVV on that day. 6 months later, I’m down 15%. That’s not cool. That’s my first 6 months out of work and my $10,000 that’s supposed to be my hedge is now worth $8,500.

6 months after that, I’m ahead by 11%. A year later, I’m up 20%, and then today, I’m up by 621%

Hedging – Getting started

Investments like a nice low-cost S&P 500 fund, or an oil price hedge like Conoco Phillips are not just for our retirement account.

With only a few clicks, we can open up a brokerage account at Fidelity, Vanguard or Schwab, move some money in from our bank account, and buy securities.

Setting up the account is free, trades are mostly free, and we can do it all from the comfort of our own couch.

We don’t need to invest millions. We can start with $100, or $50, or $10.

Prices are high. And we’ve seen this play out. Today it’s gas, at various times it’s been bacon (gasp!), eggs, lumber…you name it.

Having some investments in a brokerage account, outside of our retirement savings can be a good way to protect ourselves from the impact of price increases.

And Another Thing

Expecting the Unexpected…that’s what a hedge is about.

Today, the market is up another 1/2 a percentage point. The S&P 500 is up 8.5% since April 1st. That’s 3 weeks ago!!!

We’re still at war. Inflation is up – we just talked about that. And we still haven’t resolved the DHS funding. And I’m not sure when funding runds out next, but it can’t be too far away, so another full shut-down is likely looming. But despite that, the market’s on fire.

Be ready for anything because who knows what’s to come.