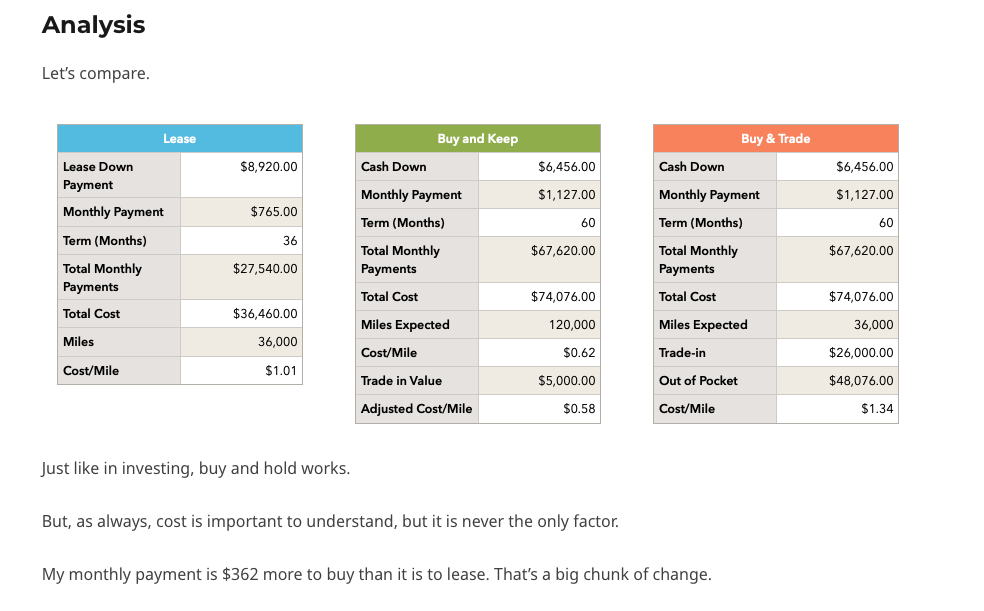

I wrote a post a while back about the financial implications of buying v. leasing a vehicle. Check it out here. And if you want to cut to the chase, here’s the calculated cost per mile under 3 scenarios.

Out of Pocket

While financially, it seems like the right thing to do is buy and hold onto the vehicle, Tony reminded me at lunch yesterday that this is not always financially viable.

Inflation is not transitory. It’s stubbornly high. Just ask Reuters.

Vehicle prices continue to rise. The average cost of a new vehicle is about $50,000.

Interest rates remain higher than they were pre-pandemic.

The Case for Leasing

Perhaps my budget will be better served by a lease?

- My upfront cost will likely be lower

- My monthly payment will likely be lower

- I’m avoiding sales tax

- If I lease a vehicle that maintains its value and I treat it well, I could buy it back at the end of the lease

While I still stand by the cost per mile figures and my position that buy and hold is the better option over the long term, I have to agree with Tony that there are times when a lease may make sense.

If that upfront payment or the monthly payment is putting our budget at risk, it may make senes to lease.

Let’s say our monthly payment is a couple hundred dollars more than our lease payment. If we occasionally need to accumulate some credit card debt (at 29% APR or higher) in order to make our budget work, we’ll quickly erase any savings that buy and hold provided.

Grok

These days, I don’t make any decisions without consulting Grok.

Grok:

- Helped me plan my vacation

- Created a detailed Roth conversion strategy for me to minimize taxes

- Helped me find 3 reputable gutter replacement contractors and reviewed/evaluated each of their quotes to get me the best deal

- Analyzed a problem with my freezer’s ice maker and provided recommendations to resolve

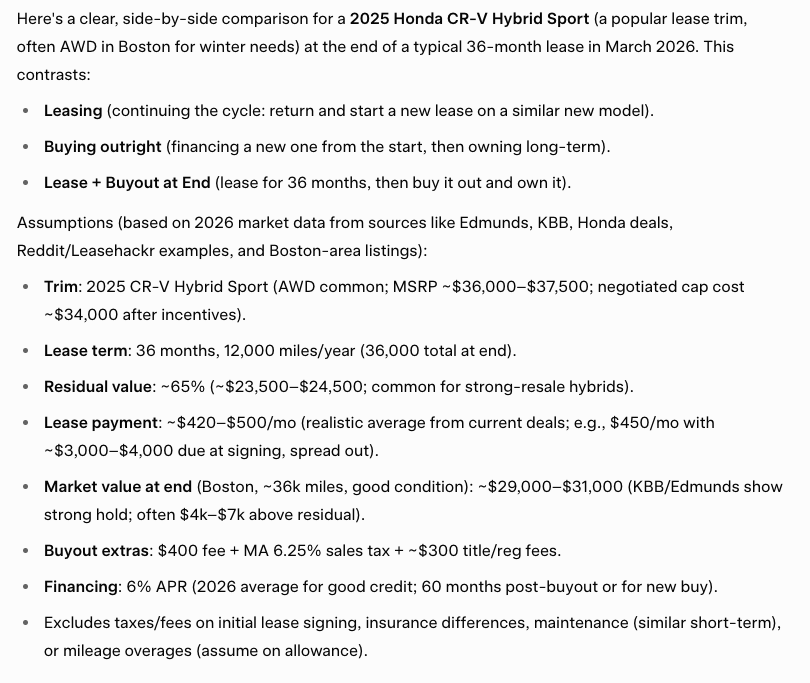

So I decided to put him to work with the buy v. lease evaluation. We chose a popular vehicle with solid resale: a 2025 Honda CR-V Hybrid Sport

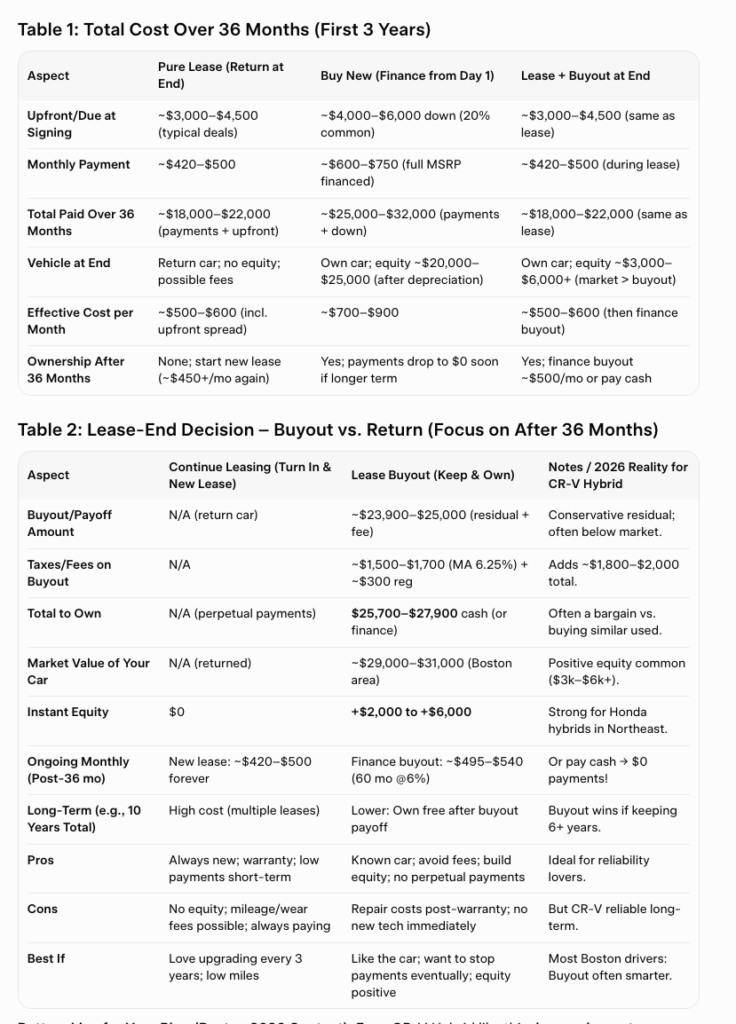

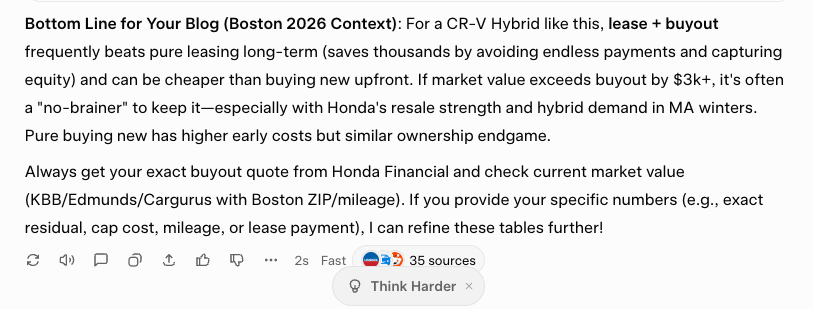

Here’s What Grok Had To Say

This is why we should never make a decision without consulting our favorite AI assistant. The tables above were the result of a conversation with Grok. I asked some info, he asked some follow-up questions, and Bob’s your uncle.

My conversation with Grok started with a simple “should I buy v, lease”? I got some generic info and Grok then offered “if you’d like to share your location and the vehicle your considering, I can get more specific.” Before I knew it, I had a detailed comparison to bring with me to the dealer.

For my gutter project, Grok provided me text to cut and paste into an email to politely get warranty specifics, revise contract wording and reduce prices.

Wrap Up

There is no one-size-fits-all for any finance decision.

However, a new vehicle (or used) is a huge financial decision and requires some homework before we jump in.

Most importantly, leverage the expertise of AI. AI is not perfect, but what it will do is hunt down every website that has information, read thoroughly and summarize what its found. For my gutter companies, it read through Google reviews, Reddit, Angi’s list and several other sites. It read every review looking for red flags.

How many of us go beyond reading/skimming one or 2 reviews on a single site?

If we’re considering buying at the end of the lease, consider residual value. What will our new vehicle be worth in 3 years? A Honda CR-V loses a lot less value than a Jeep Wrangler. AI can help here as well.

And if we’re getting into a long-term relationship with a vehicle, make sure it is a vehicle that will be reasonable to maintain, and that we’ll be happy to hold onto for 10 years. I have some thoughts on this here.