I’ve spent quite a bit of time searching for credit card rewards. A few years back, I was getting a new credit card every few months in order to get airline miles, hotel points or other rewards.

It was fun. I felt like I was traveling for free.

One Big Caveat

Here’s the warning…This only works in your favor if you pay the balance off each month. Typical reward cards charge 20%-30% APR. This will eat away at any rewards very quickly. So for this post, we’ll assume we pay 100% and do not carry a balance month to month. And don’t even get me started on the $40 or so late payment fee…

Sign-Up

Sign-up was easy. My wife and I both have great credit scores, so I’d go online, fill in some info and soon I’d have a new card. Typically, I’d have to spend $4,000 or so in the first 3 months, and then I’d get the points, miles, or hotel nights.

Card Example:

Like this:

What Does That Get Me?

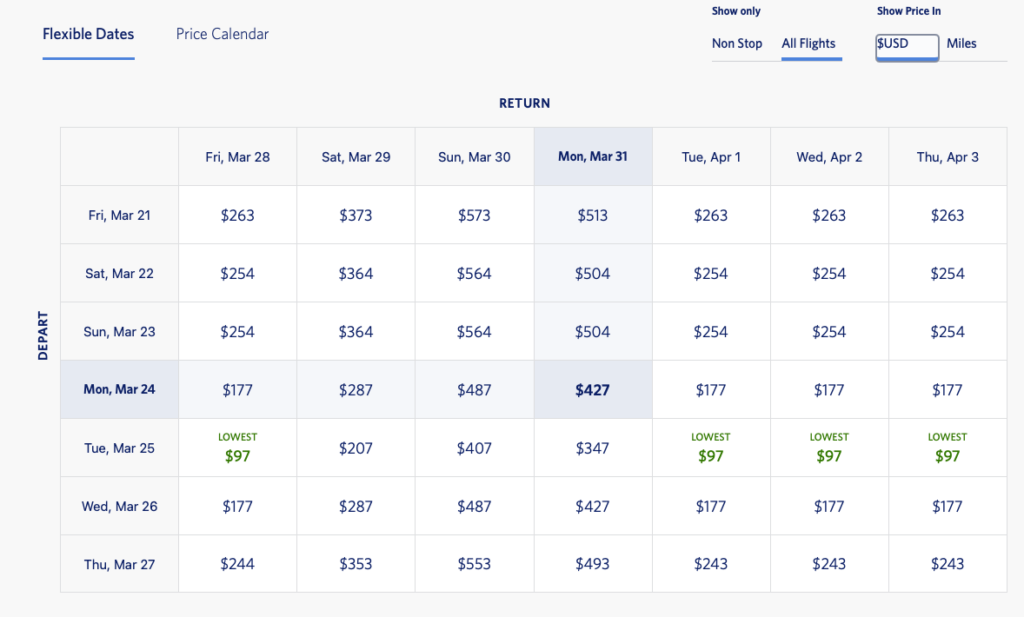

Let’s use Delta as an example. Looking at Delta’s site, I can get a round-trip coach ticket to Miami from Boston for between 18,500 miles and 48,500 miles. If I book further out, I can get down to about 15,000 miles.

or Dollars:

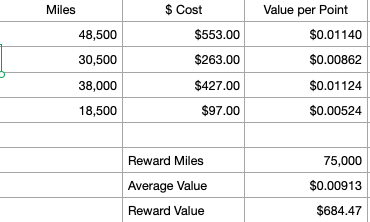

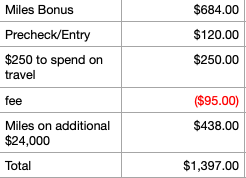

Quick math tells me the average value per point is about $0.0913. So the value of the 75,000 points is roughly $684. The points are worth more on a more expensive flight.

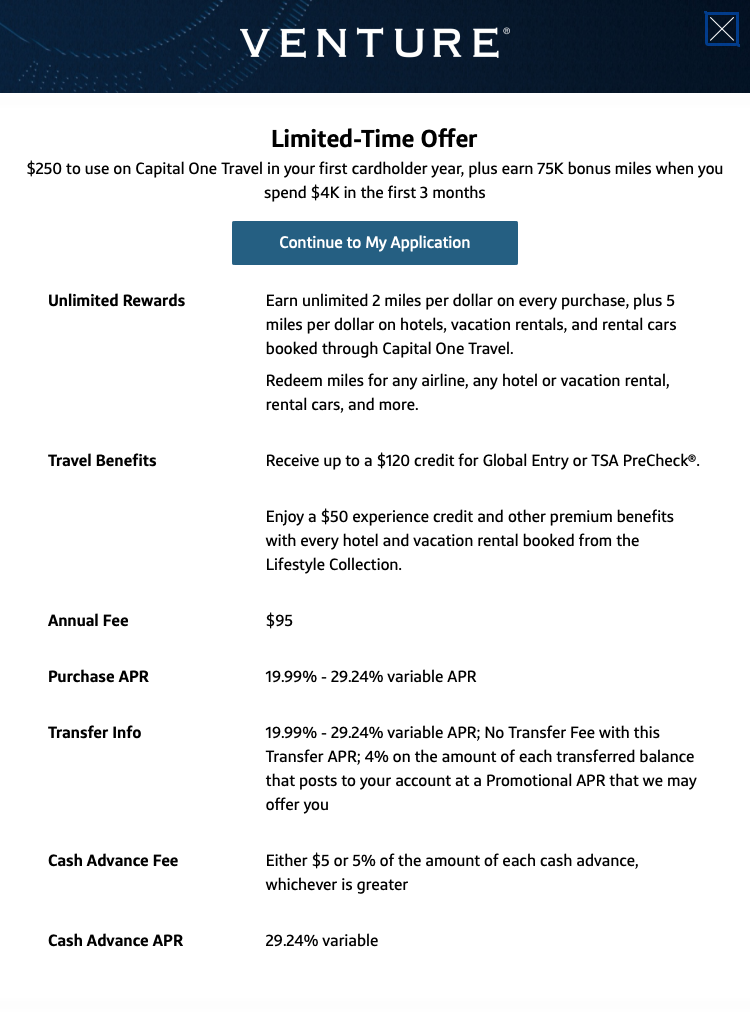

After the initial bonus, I earn 2 miles per dollar spent. Here are the details:

It’s a nice offer. I get a credit for TSA pre-check or global entry, $250 to spend on travel, and 5 miles instead of 2 for spending on vacation.

The interest rate is predatory, but that’s true for most credit cards, and it looks like the $95 is not waived for the first year as it is on some deals.

All-In

In order to tell if this is a good deal, let’s look at the total benefit. Let’s assume that I put a lot of stuff on my credit card each month and pay it off at the end of the month. I spend $2,000 per month, or $24,000 per year.

With the 2 miles per dollar spent, that nets me an additional $438 on the $24,000 spent.

Here’s what the total looks like:

Not bad. I change to a new card, and I end the year with $1,397.

Cash Back Rewards

After trying a dozen or so deals, and getting some pretty neat discounted trips, I took a look at boring old cash back rewards.

I have 3 different cash back cards: My Fidelity Signature Visa, my WellsFargo ActiveCash Card and my Citi DoubleCash card.

There are lots of cash back deals around. Discover offers an interesting one where they match points 1 for 1 the first year, essentially doubling cash back, and each quarter they announce 2 types of spending that get 5% cash back instead of the usual 1%. For example, this quarter, Discover card holders get 5% cash back at Grocery stores and wholesale clubs.

I lied (a little). I do also have the discover card and I only use it for the 5% cash back items.

The reason I lied is to keep the math simple. My 3 other cash back cards all give me 2% cash back. Note also that none of these cards have an annual fee.

My cash back rewards, assuming I spend the same $24,000 are…drum roll…a measly $480.

Cash Is King My Foot

Would you rather have $1,397 or $480? Is this a trick question???

I choose the $480. While math is not my strong suit, let me explain.

Travel Rewards and Me

My golf buddy Rich has the JetBlue card

Rich travels very frequently. He uses all of his miles on trips that he’d be taking anyway. Go Rich.

My wife and I flew to Florida in February. It was the first time in over 5 years that either of us had flown. We used points to book the airfare. I still have over 200,000 miles waiting on our next trip.

In 2021, my wife, Rosco and I drove to Florida. I used some hotel points to book some one night stays along the way, but we used AirBnB and Vrbo to book houses for our longer stays.

If I earned over 100,000 miles on a new credit card like the Capital One Venture card, 2 things are likely to happen.

- My wife and I book a trip we had not planned to book in the first place – we have free miles why not?? We get a free flight, but we shell out for hotels, restaurants and activities that we wouldn’t have spent on otherwise.

- The miles sit unused waiting for our next planned trip. While many airline miles don’t expire, some do, but almost all lose value pretty quickly.

For me, the $1,397 savings is likely to make me spend more.

The $480 is cash. It shows up regularly in my checking account.

Wrap-Up

So for me, after trying quite a few cards, I realized it was more fiscally responsible for me to stick with the cash back rewards. However, my buddy Rich is saving big with his JetBlue rewards because he’s going to travel anyway and the points more than offset what he’d get with 2% cash back.

These incentives often push us to spend money on something that we wouldn’t otherwise spend. For me, I like taking the cash.

Marketers and retailers are smart – much like criminals (apologies to any retailers or marketers who are reading). They know what attracts us. We love a deal. And who doesn’t like to travel?

We sign-up. We try and maximize the points, then we start to carry a balance, on which we pay insane interest rates, and all of a sudden those points they gave us are a cheap incentive to get us to continue to pay 29% on our outstanding balance.

Credit cards and the rewards they offer can be a nice benefit to us as long as we pay in full each month. But even if we do, we need to make good decisions about which rewards are most beneficial to us.

Read more about credit cards and how they work here.

Footnote on Credit Score

At the point where I was applying for a new card every few months, my credit score took a hit. It also took a hit when I closed cards after a few months because average length of credit accounts goes down. Read more about credit scores here.