Investing is a hobby for me. I’m retired and I’ve got lots of time. Why not?

2026 has been a wild year, what with AI, the war in Iran, and lingering inflation, but I find it interesting that the lessons from prior years still hold true.

Bitcoin

I’m a bitcoin skeptic.

I understand stocks. I buy shares of a publicly traded company like Amazon, Starbucks or Walmart. I know who the CEO is. I can visit the company’s website. I can go to my brokerage platform and read investor reports on the company.

If I’m really motivated, I can read the annual report and the 10-K and look at sales, earnings, debt, return on equity, and other metrics that will tell me how my company is performing v. similar companies.

Bitcoin though…the price goes up, it goes down…why?

On 2/3/25, I invested $8,704 in a Bitcoin ETF Ticker: BTC. Here’s what Bitcoin has done.

And here’s what that means to my $8k gamble.

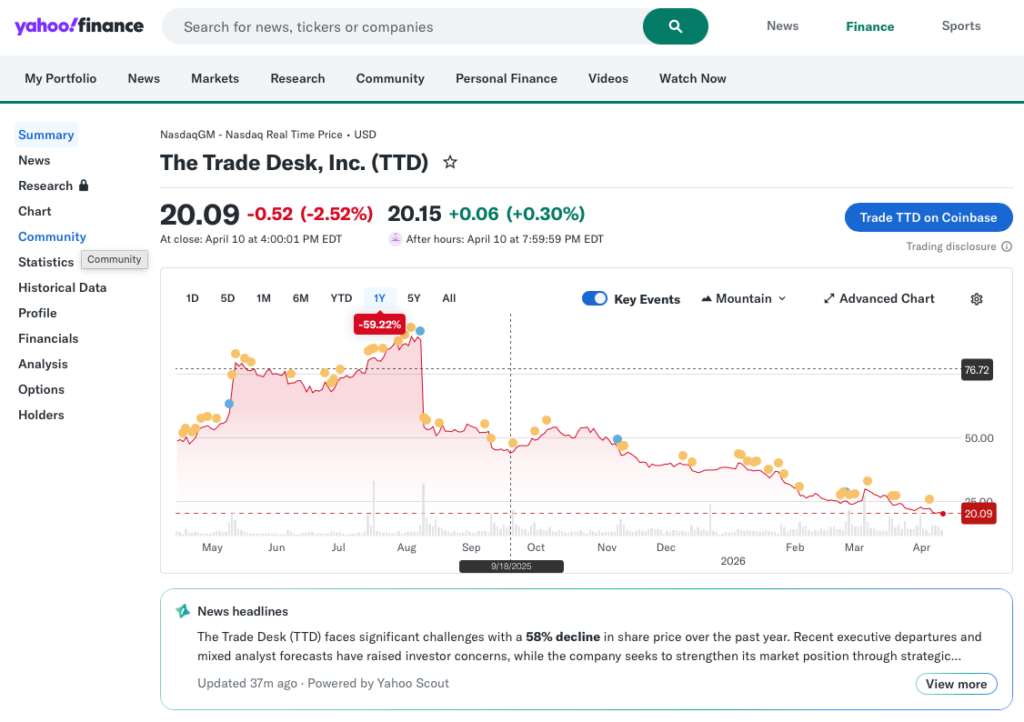

I own shares of an online advertising company called The Trade Desk, ticker: TTD.

I’ve lost money on the trade desk over the past year. Much more than I’ve lost on Bitcoin.

Tech stocks in general have gotten whacked due to concern about AI replacing everything. Competition is tough. The Trade Desk is up against Google and Amazon. Executive departures can be a sign of trouble.

I can see why it’s down, but I also have reasons to expect it will recover. It has almost no debt. Sales are increasing. Existing customers are spending more with them each year.

I may be right to be optimistic, I may be wrong. But I can evaluate some business results to make my own assessment.

With Bitcoin, I’m hoping other investors get excited and start buying more. I have no idea what might make them more excited, and even if I did, I don’t know when that catalyst may happen.

To me, Bitcoin feels like a gamble.

I opened a small position so that I could watch and learn. I’ll continue to do both, but the past 14 months have only reaffirmed for me that Bitcoin is gambling.

Stocks

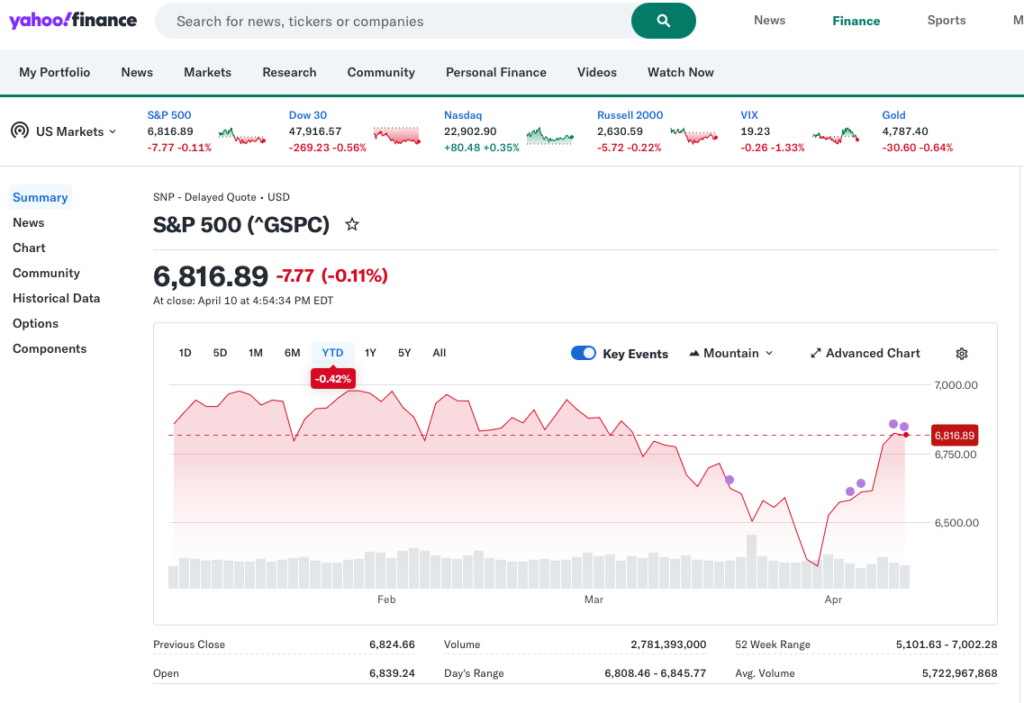

The market – specifically the S&P 500, continues to be volatile and unpredictable in the short term.

Today we have war in Ukraine going on year 5 (yup, it started in February 2022). A new war in Iran. The market moving 2% when our commander in chief decides to post to social media at 4am. Yup, volatile.

With all this, the S&P 500 is only down 0.42% YTD.

But, where tech stocks like Alphabet (Google parent), Microsoft and Amazon have been huge growth drivers for the S&P, this year, many are down or flat.

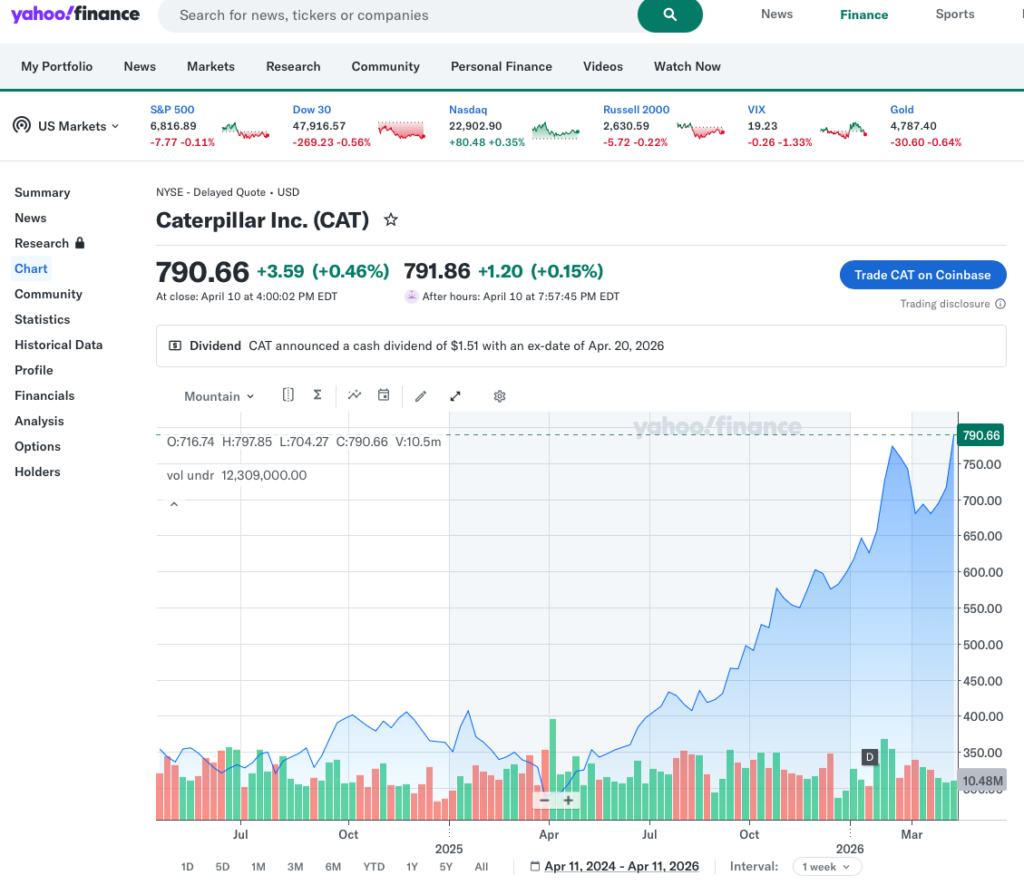

The biggest shocker in my portfolio is Caterpillar. It’s up 38% YTD. Look at the 2 yr chart.

I bought shares in 2023 that are up over 184%. This is a large equipment manufacturer. Not an AI company. What gives?

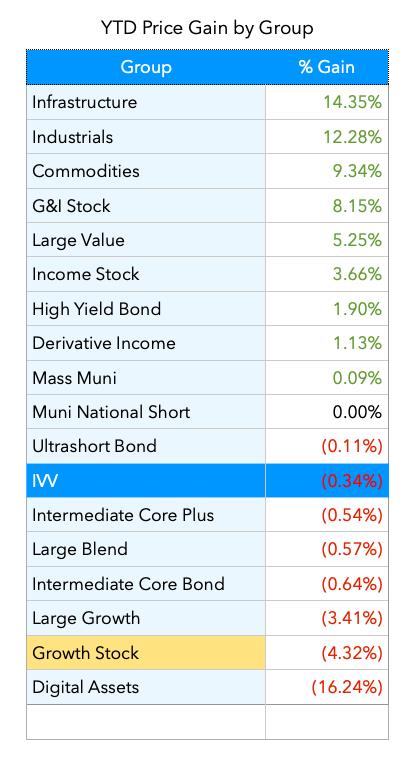

If I look at my investments by group, the growth stocks that have driven the lion’s share of my earnings for the past 20 years are lagging – big time. This year Caterpillar, Cummins, Fastenal and Carrier are killing it.

Diversity matters. This doesn’t mean we need to hunt for small cap Asian emerging market companies. It could mean that we need to own companies in different sectors of the US market so that when one sector pulls back, we own companies in other sectors that will compensate.

No company’s stock price goes up daily forever. There will be pullbacks. We don’t know when they’ll happen, we don’t know how long they’ll last.

Having a diverse portfolio likely means will have some winners even in crazy times.

Income

Income is nice.

The best part of working is knowing that they’ll be a paycheck coming every 2 weeks or so.

I’m retired, so no more paycheck. And as much as I’d like them to, the bills won’t pay themselves.

So it’s up to my investment portfolio to provide income.

While I was working, my portfolio was growth focused. Amazon, Netflix and Apple had a large place in my portfolio. Now that I’m retired, I’ve rotated into investments that generate some income.

This has been a slow rotation. It started in 2018 – a year before I retired, and it’s still in-progress. I’ve sold a lot of growth stocks. I’ve bought shares of companies like Waste Management, T. Rowe Price, Prudential, Safety Insurance, and Bank OZK, that pay a nice dividend along with their growth potential.

As a group, I expect these companies will lag the S&P 500. I’m hoping for a small capital gain over the next 20 years. But even no gain is fine. Today, a few of the companies have had gains, a few have had losses. That’s OK, because each pays me a quarterly dividend.

Safety Insurance pays $3.68 per share per year. That’s a 4.92% annual return just on the dividend. Some cap gain would be nice, but if it keeps paying me 4.92% every year but stays flat or loses a bit, that’s OK.

I also have some bond mutual funds. Lots of them. We’ll talk more in a sec, but I have the same expectation for my bond fund investments. I’d love some gains, but their job is to provide a monthly income stream.

Bonds

Bonds are tricky. Other than US Treasuries, I don’t buy individual bonds. I prefer to invest in bond funds and ETFs that track an index, or have a portfolio manager that makes buy and sell decisions for me.

Interest rates are a huge factor in bond returns. Rates were supposed to be going down, but now it looks like the Federal Reserve is considering a rate hike. I don’t totally get it so let’s leave this to the professionals.

That said, I like to diversify my bond fund holdings a bit.

Dividends

With a company that pays a dividend, that dividend is pretty dependable. Companies tend to try and grow their dividends. It is pretty rare for an S&P 500 company to cut its dividend. It happens, and it happened to companies that I owned like Intel and VF Corp. It’s a bummer and often a sign of trouble.

But in general, companies like to grow dividends. Dividends are paid to shareholders. Who holds the most shares? The folks running the company. It’s in their best interest to keep growing the dividend.

And we keep track. The Dividend Aristocrats and the Dividend Kings are lists of companies that have grown their dividends for many years. If I’m a dividend aristocrat and I’ve just joined the list by increasing my dividend payout for 25 consecutive years, do you think I’ll increase my dividend this year? Would I risk dropping off the list and starting again? Probably not.

However, just because our bond fund pays 4.45% today, this is no guarantee that it will pay 4.45% tomorrow, or next year.

When interest rates are on the rise, new bond offerings will pay a higher rate. When rates are declining, new bonds will pay a lower rate. Bond fund managers are trading bonds daily in anticipation of rate changes and to try and maximize total return (capital gain + rate).

Because rates are volatile, it pays to have a diverse portfolio of bonds. I hold some high yield (junk) bond funds because they pay a much higher rate. But I offset this with a much larger portion of my bond portfolio in ultra-short term bonds. Ultra short bonds have durations of less than a year so they are less likely to be impacted by interest rate changes.

But the bottom line here is that I’ve traded some long-term capital appreciation potential for a regular income stream. I still hold some growth stocks, but I have a lot more of my portfolio in income-producing high dividend yield companies and a diverse collection of bond funds and ETFs.

Patience

Today I took a look at the companies that I’ve invested in and the time I’ve been invested.

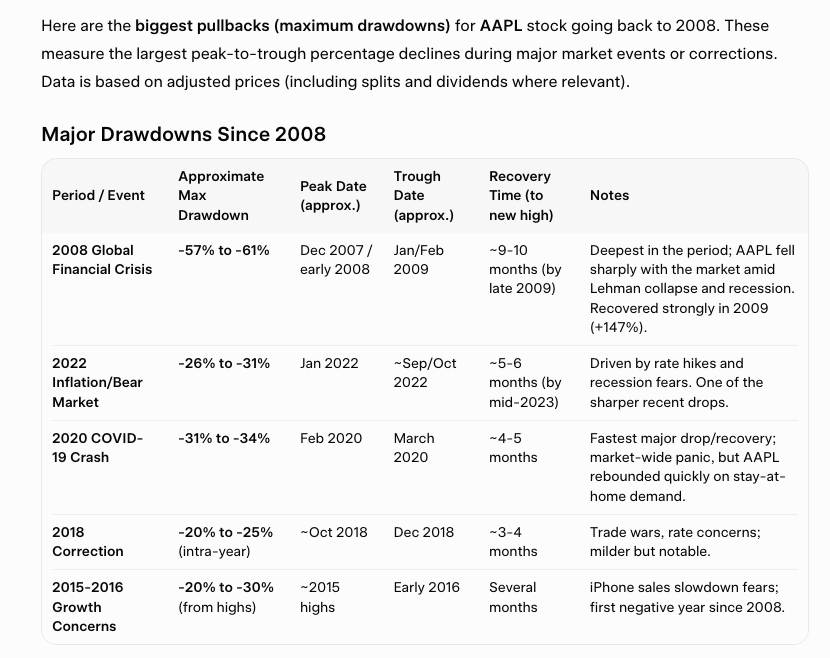

My oldest active holding is a 2008 investment in Apple.

It’s easy to look back now and say this was a great investment and why didn’t I invest more than $1,257.

But there were some really bad years for Apple. I asked Grok.

So right off the bat, I invested in Feb 2008 and look what happened.

While I held onto Apple and watched it take-off from 2009, I sold quite a few favorites like Amazon, Netflix, Disney, Starbucks and Costco. I bought back in later at much higher prices and am ahead today, but if I’d just been patient…

I had a similar experience with Amazon. I bought more shares in 2022, and saw the value of those shares drop by more than 50% in 2023. I bought around $170 per share, watched them drop below $80, and today Amazon shares are at $238.94.

I can cherry-pick examples where selling a stock was a great idea. I lost money on both UPS and Whirlpool and eventually sold shares. Both companies have continued to fall. UPS is down over 30% since I sold, and Whirlpool is down over 40%.

But if I look at all sales, I would be better off today if I’d never sold, because Twilio is up 85% since I sold, Ollie’s Bargain Outlet is up 76% since I sold, and I sold some of my Nvidia holdings early on. Had I held on, they’d be up over 1,200%.

One Nvidia makes up for lots of UPS and Whilrpools.

Wrap Up

Bitcoin, Diversification, Income and Patience. 4 lessons for April 2026.

Bitcoin is a broader lesson. I can’t figure out how bitcoin will make me money. It doesn’t have any of the attributes like a business has that help me understand why it might be more valuable in the future. And it’s not like a home or investment property. I can live in a home. I can rent out an investment property. I can understand why they’re valuable. Bitcoin???

Diversification. We never know what the market is going to do. Even our best investment ideas will struggle at times. Owning a diverse group of assets in our portfolio helps us to weather those pullbacks.

And all of us will get to a point where we’ll want our investment portfolio to start paying us. When the paycheck stops, it would be great if we could rotate into a suite of investments that will provide some potential for capital gain, but whose primary focus will be to provide a dependable income stream.

Patience. This is the toughest. When one investment is down, or lagging, there is always another investment out there performing better. We could sell today, get out of a losing position, and get into that investment my golf buddy keeps bragging about.

And while it often provides some relief to get our of a losing position and to no longer see that red on our scorecard, 10 years from now, we may look back at that and recognize a mistake. And especially if we have a diverse portfolio, our investments as a group will perform differently in different economic situations, but if we’ve done the work to build a thesis, more often than not, hanging in is the best plan as long as that thesis holds.