I’ve read and written a lot about investor mentality and about the difficulty of staying the course during a market pullback. None of us like to lose money. Logging in to our financial account and seeing a huge dollar drop is a bummer. When it happens day after day, it becomes draining. We feel like we need to act.

I know this. During the 2008 melt-down, I lost my job, and my daughter started college. I dumped stocks and moved to cash because I couldn’t watch my account value sink by thousands of dollars every day. I had no job and college payments were starting. Yikes!

In hindsight this was a terrible decision. As it always has, the market recovered and then went on to new highs.

Not Your Fault

Yesterday I was reading an article by Morgan Housel who writes for the Motley Fool. I like his writing. He puts market meltdowns in perspective and provides facts that help me stay invested when I feel like I should be selling.

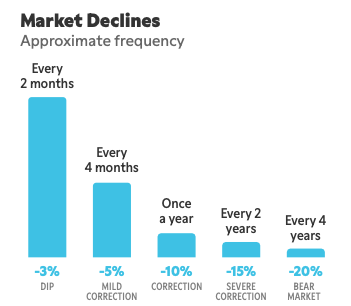

In his most recent article, Morgan states something that I hadn’t heard anyone say before. I’m paraphrasing, but what I got from the article is that we, as investors, didn’t do anything wrong. The market is tanking, but it tends to do that fairly frequently. Volatility is the price of admission. While the broad market (think the S&P 500) builds wealth over long periods of time, we know from history that it will pull back 10% or more very regularly, on average, once every 11 months.

And because we didn’t do anything wrong, we don’t need to take action to correct anything.

What Should I Do?

I like this. My first reaction when there is a problem is to ask myself what I need to do. And my retirement balance dropping each day certainly is a problem. So therefore I must need to take action.

I’m pretty good at stopping myself. The 2008 meltdown taught me that. I could have retired years earlier if I hadn’t sold.

But I still go through the thought process. What should I sell? Am I over-allocated to equities? Should I buy to take advantage of lower prices?

Should I Sell?

No

I review my holdings regularly and update my thesis for each investment. I had nothing I needed to sell in January so in case something (other than the price) has changed, stay put.

One exception…Tariffs. While tariffs will likely be short lived – months or years, not likely decades, they may have a big impact on some industries. Tariffs are something that has changed.

I believe the companies in which I invest are the best choices in their industry and they are likely to gain market share from competitors in tough times. Many of them have proven to do just this in prior pullbacks.

But I am concerned about housing. The US has been short on homes since the bubble burst in 2008, but it seems like every time I test the waters with a small purchase of a homebuilder’s shares, I lag the market. Homebuilding just doesn’t seem to get its act together.

So adding in the tariff headwinds, I took the opportunity to sell some shares of a homebuilder. I had made some gains, but I sold 1/3 of my position (at a profit) to reduce my exposure.

Am I Over-allocated to Equities?

No again.

I looked at this in November of 2024 and made some adjustments. I reviewed my cash needs to support our spending, and moved a bit more into fixed income because rates are high and it’s a nice source of regular income.

I was happy with this allocation then, so why change it? When equities are down, it’s not the time to sell. This is why it is important to review our asset allocation regularly and make moves when the market is in our favor.

Should I Buy?

Ever heard the expression “don’t try and catch a falling knife?” Spoiler: you’ll get cut. I’ve never had a good experience buying during a market drop. Boy does it hurt when the stock I bought when it pulled back 10% drops another 40%.

My exception to this rule is regular investments. For those who have a 401k or other defined contribution plan, you’re making investments every time you get a paycheck – whether the market is up or down. And for those like me who reinvest our dividends, Every quarterly dividend buys more shares. When the market is down, we’re getting more shares at a lower price.

Price of Admission

So, Morgan says volatility is the price of admission. Here’s a nice little chart that shows how often the market declines based on data from the past 45 years.

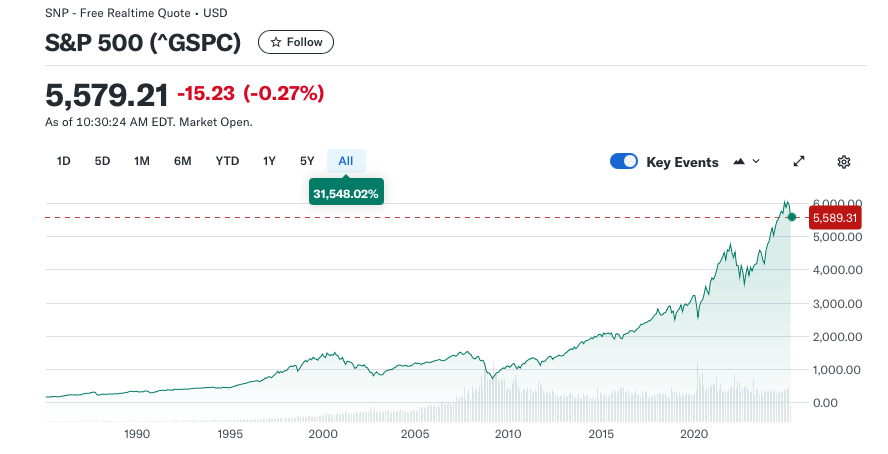

Here’s a chart that I like better. This is the S&P 500 price over the past 37 years.

You can zoom out and see some ups and downs, but overall, it’s been up and to the right.

Read more about the S&P 500 performance here.

Wrap-Up

Volatility is the price of admission.

There will be 10% pullbacks, which is roughly what we’ve seen in the last 6 weeks, fairly often. We’ll also see some pullbacks of 20% or more, and we should not be surprised to see our equities lose half their value at some point in our investing career.

The S&P 500 has been a wealth-building machine over long periods of time. Volatility is the price we pay to participate.