Mutual funds and their close cousin the Exchange Traded Fund (ETF) are great for investors. We get instant diversification and we get the benefit of either professional portfolio management (for an active fund or ETF) or we track an established index for a passive fund or ETF. Either way, we’re getting some help in selecting investments.

While there are some differences in how a mutual fund operates v. an ETF, they are both a basket of securities. We buy shares of the fund or ETF, and the fund or ETF can hold dozens or even hundreds of stocks, bonds, or a mix of securities.

No Such Thing as A Free Lunch

As an investor we get diversification and management, but like anything else in life, nothing is free. While we don’t explicitly pay the fund company, a small portion of our returns goes back to the fund company to pay its expenses.

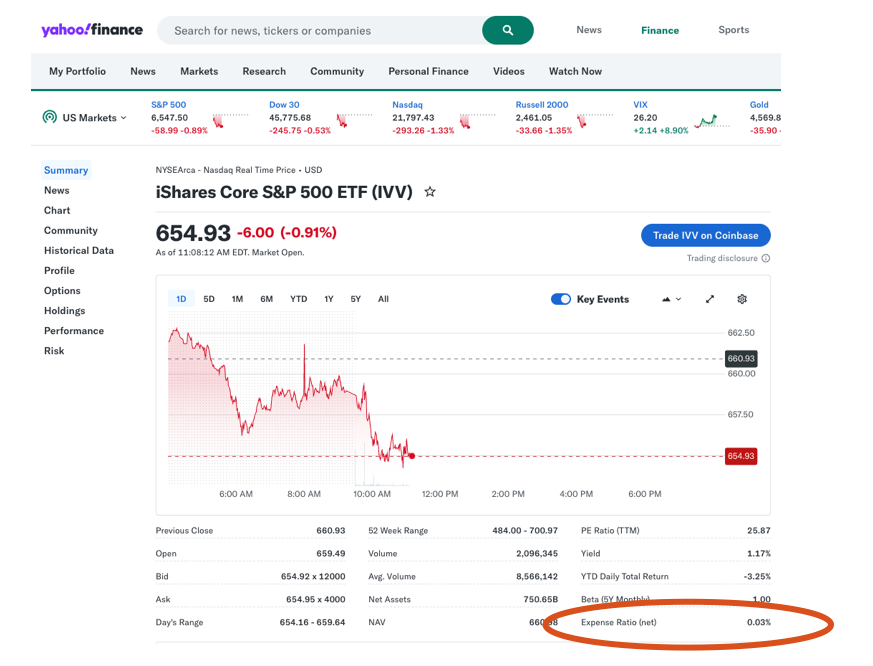

Every fund is required to report how much it charges in fees. We can see this on Yahoo Finance. It’s called the Expense Ratio.

In this example, the iShares Core S&P 500 ETF charges a fee of 0.03%.

This means that for every $10,000 we invest, we’ll pay $3 per year. Pretty cheap, huh?

Even if we have $100,000 invested in the ETF, we only pay $30 per year.

Mutual funds and ETFs are a great deal. Because costs are spread out across thousands of other fund investors, our cost is pretty low.

Cost Matters

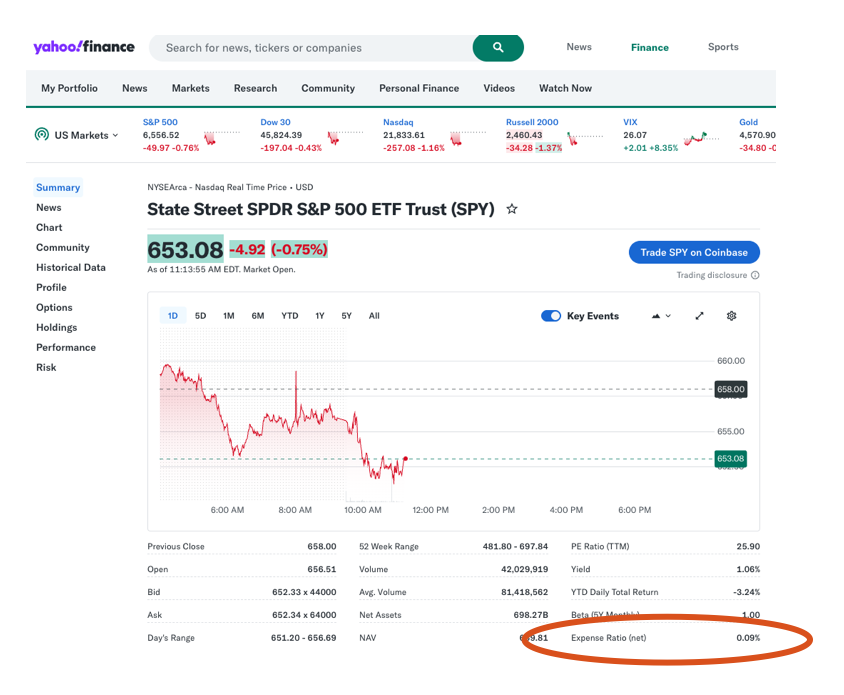

We’ll talk about why in a sec, but first take a look at the State Street SPDR S&P 500 ETF

It has an expense ratio of 0.09%. That’s 3x what we’d pay for IVV.

OK, we’re talking $9 per $10,000 invested v. $3…That doesn’t even pay for a meatball sandwich.

But, let’s take a look.

Fees Eat Away Returns

Let’s take a look at the FINRA Fund Fee Analyzer. That will be fun!

FINRA is

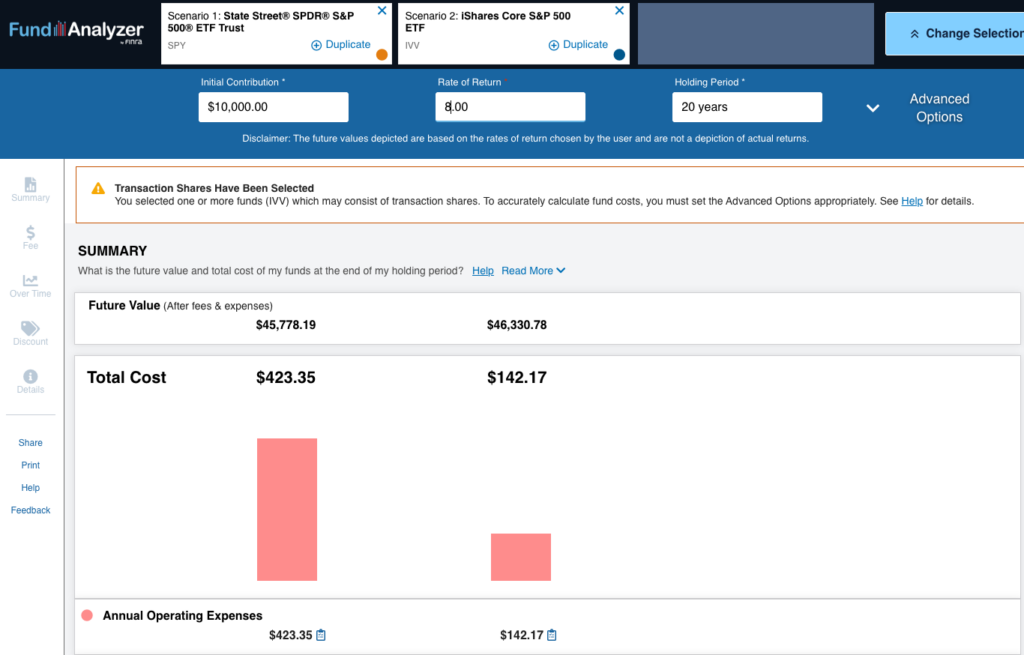

Here, I’m taking a look at what we’d pay in fees over a 20 year period assuming an 8% return.

I’m comparing SPY to IVV.

We’d pay an extra $281.18 in fees. But more importantly, our ending balance would be $552.59 less because as those additional fees come out each year, we lose the compounding effect of the additional fee amount.

In this example, we are comparing 2 S&P 500 ETFs. They both invest in the exact same 500 companies in the exact same ratios. Why not buy IVV and have an extra $523 in your pocket in 20 years?

But…

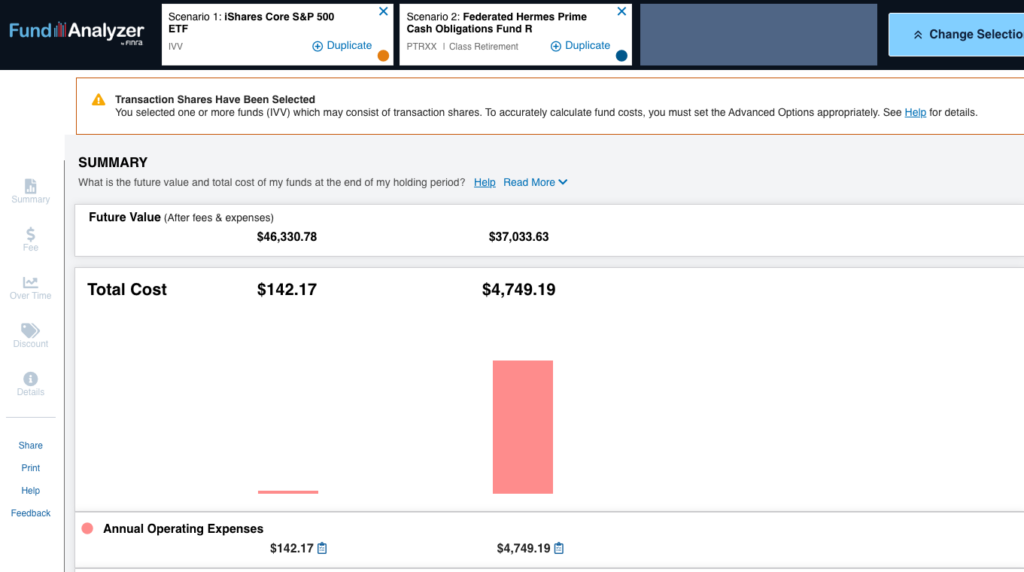

This get’s even more pronounced as we start to look at the difference between actively managed funds, which typically charge higher fees, and index funds.

In this example, we have a fund that charges 1.15% v our 0.03% IVV.

Now it makes a difference. We would have nearly $10,000 more after 20 years, assuming they performed equally.

Wrap Up

Fees make a difference.

When shopping for funds, if the fund invests in similar geographies, sectors and companies, it’s almost always best to choose the lower expense ratio.

And with index funds that invest in the same index, it’s a no brainer. Pick the lower expense ratio.

Today, I was surprised to find that one of my favorite mutual funds has an ETF version. The ETF has a .14% lower fee. Guess what I did this morning? I put in sell orders for all shares. Monday morning, I’ll buy shares of the ETF version.

And to follow-up on the comment about active v. passive. Active funds typically have a higher expense ratio than a passive fund. This is because the fund company needs to hire a portfolio manager to make investment decisions and a research staff to inform the portfolio manager.

And research ain’t free. They need to pay for that so the portfolio manager is getting the best timely information.

To launch an index fund, the fund company subscribes to the index, buys shares of all the companies in the index, packages them in a fund and pretty much calls it a day. Not a lot of expense.

And the actively managed fund needs to beat the index in order to offset the cost of its fee.

Something to consider.