Unless we end each month with more money than we know what to do with, we need a budget. If that sounds like an exaggeration, it’s not.

Why Do We need a Budget?

Before we talk about the mechanics of creating and managing a budget, let’s talk a little about why we need one. Most of us work for our money. Many of us work 40 hours a week, or more. We might rather be spending time with kids or grand-kids, playing golf or lying on a beach, but those things aren’t going to pay for our rent/mortgage, our grocery bills, or help us save for retirement. So instead, we get up every day and we go to work. Many of us claim to love our jobs, but would we still go if they stopped paying us? Probably not.

We spend a good chunk of our waking lives working. The main purpose of which is to get a paycheck to help us support ourselves and our families. Given the effort we put in to earn our paycheck, doesn’t it make sense that we would want to maximize the benefit we receive?

My wife and I have built a lot of stuff at our house – patios, decks, gazebos, cabinets and shelves. It’s taken a lot of work to build them so we continue to invest a lot of time and effort to maintain them. Think of your paycheck the same way. We’ve put in a lot of work to earn that salary. It seems worthwhile to spend some additional time to ensure we receive the most value for our time spent.

A budget is an important way to do that. A budget enables us to decide how we are going to spend the money that comes in before we spend it.

You’re probably saying “yeah, right. I have all these bills that need to get paid. How does a budget help?”

Here’s how.

Budget Step 1: Start With a List

We start with an inventory of all of our income, and all of our expenses.

We’ll talk in detail about how to do this shortly. Hang tight.

We may find that our expenses exceed our income. We’ll get to that. At this point, we’re just collecting the facts.

Once we’ve got the inventory, we can then start to make decisions.

There are really only 2 types of decisions most of us can make. We can get more income – take a part-time job, drive for Uber, put the kids to work and let them contribute… or we can reduce expenses – turn down the heat, turn off some lights, carpool, hunt for cheaper insurance, cell phone plans, etc. We can get radical and try to survive with 1 car instead of 2. We could downsize our home.

Make Choices Based on Facts

The point is, we now have the facts in front of us which enables us to make decisions. I remember about 10 years ago, I had a lot going on and I had lapsed on managing my budget. That’s OK – happens to all of us. At some point, I looked at my credit card statement and realized I was paying almost $200 a month on my home phone, internet and cable TV bundle. And that was 10 years ago.

I got angry, I called my cable company and after lots of failed suggestions, I decided to cancel home phone and TV completely.

I was angry because my negligence had caused me to pay $200 for stuff I didn’t need. I proved I didn’t need it. My wife and I have lived without for over 10 years.

I’m not going to tell you that you can’t have cable TV. That’s not my role here. I want to help you pull your expenses and income together so that you can decide. I want to help you become the decision-maker. You should decide where your money goes. The alternative is that you become a victim. You work all week with nothing to show for it but a growing pile of credit card debt. Where you choose to spend your money is your decision.

Gather your Inputs

The first step in creating the inventory is to pull up our checkbook, our bank and credit card statements, a pencil and paper and start listing all of our income. This would be paychecks, but also includes interest earnings, rental income, or anything else that comes in on a regular basis. Next up, do the same with expenses. Electric bill, gas bill, phone bill, rent/mortgage….write down the item and the amount.

Monthly Budget

I like to do a monthly budget. It allows me to keep score on a monthly basis and adjust each month. One of the tricky parts is accounting for expenses that are not paid monthly. For example, I prepay my home, car and umbrella insurance every year. I save a good chunk of money by doing this, but I need to ensure I have enough cash on hand when the bill comes due. In my monthly budget, I need to have a line item for an insurance fund in which I save 1/12th of my payment each month and put it in a separate account so that it is available when the bill comes due. Taxes is another line item. Seems I always end up paying so I need to put money aside each month.

Remember, we are just doing the inventory at this point. If this is your first time, you are going to forget things. That’s OK. You will continually find things that you forgot to account for and you’ll add them as you go. You’ll get better every month.

For anyone who finds that it is onerous pulling all of this together because you may have multiple credit cards and several bank accounts, you may want to consider using an account aggregator.

What is an Account Aggregator?

An account aggregator is a website that pulls all of our accounts and transactions together in one spot to make it easier to manage our finances. Many of them will categorize our transactions automatically. For example, if we buy gas at Shell with our credit card, the aggregator recognizes shell as a gas station and categorizes the transaction as Auto Fuel. This helps us to use the aggregator’s tools to see how much we spend in each category, do comparisons, etc. Most aggregators also offer some basic budgeting functionality.

Some aggregators are free, some are paid. While these tools provide a helpful service (I have used both mint.com* from Intuit, and fullview from Fidelity for years and have found them incredibly useful), you are making a trade-off for that functionality.

The aggregator may sell our data. While they will “anonymize” the data so that it can’t be easily traced back to us, they are gathering an awful lot of information about us. Also, aggregators need us to authorize them to pull our data from our credit card providers, banks and other financial institutions. Some will need us to enter our login id and passcode into their site, some will ask us to authorize this through our financial institution.

Either way, we need to make sure we understand how this works and what they do to protect our accounts. It’s also important to deal with an aggregator that has been around a long time. For a company like Intuit or Fidelity, they have a lot at stake to make sure our information is protected. But still make sure you do your homework.

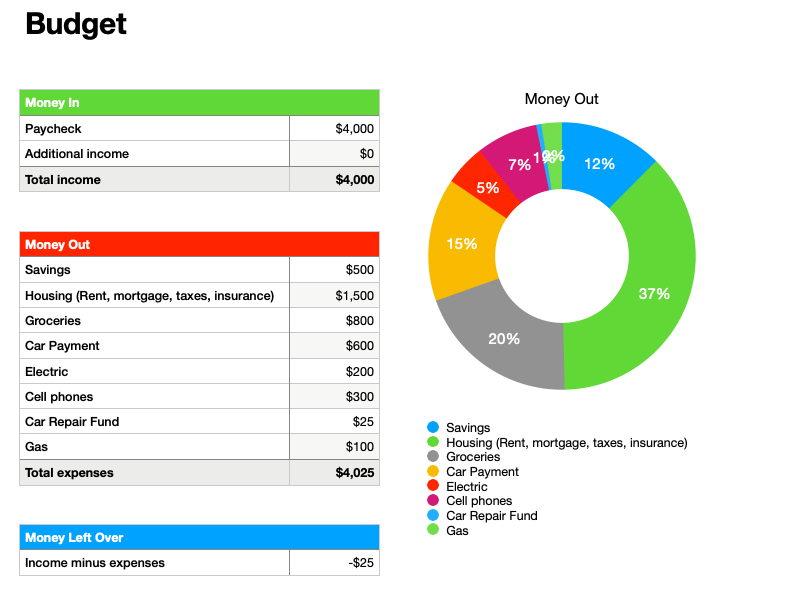

Sample Budget

By creating the inventory of income and expenses, we now have the start of our budget.

I’ve created a sample using a spreadsheet with a nice donut chart.

You’ll notice that I listed savings first. This should be the most important item in our budget. Pay ourselves first.

Car repair fund is an example of a fund we might set up to save for expenses that may not be monthly, but will come due sometime in the coming year.

What Now?

You’ll notice we are in trouble. The income of $4,000 is less than the total expenses. Our budget doesn’t work.

Had we not done a budget we never would have known.

With no budget, I’m guessing most or all of savings would not happen, the car repair fund wouldn’t get funded, and the money that would have gone here would go something else.

Now that we know our income and expenses, we can make some decisions.

A while back, my wife came home from grocery shopping. She spent $50 and got over $100 worth of groceries. She read the flyer, she bought what was on sale and she used coupons. Groceries aren’t optional, but there are ways to spend much less.

Cell phones are a big chunk of the monthly expense. Many of us survived in the days before cell phones existed. This could be an area to save.

Be creative. There are lots of ways to save. Check out our post on saving. Don’t be afraid to try some and see if they work for you. You can always go back if they don’t.

Get the Whole Family Involved in the budget process

I also encourage you to get your entire household involved in the process. I have one friend who put an expense sheet up on his fridge. He, his wife and his kids have to write any expenses here for all to see.

It’s really hard to do this alone. Everyone who makes spending decisions or who has the ability to request us to spend on their behalf, needs to be involved.

A Budget is the First Step

A budget is going to take a little bit of work to set up, but once we’ve done this, we will be able to make decisions about where our money goes. This is a good first step to help us get out of debt, to save more, and most importantly, to make sure the fruits of our labor are going to the places we want them to go.

As always, I’d love to hear your experiences with budgets, your questions and suggestions.

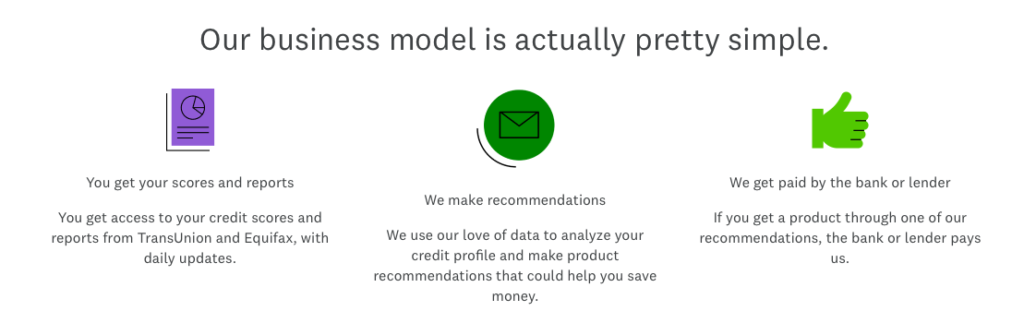

* Update 2/9/24….I received an email today that I needed to migrate my mint data to CreditKarma. I remember reading a while back that Intuit had purchased Credit Karma. I had done a cursory review of Credit Karma’s site a few years ago as I was preparing material for a class. I liked what they provided. See below for their info regarding their business model. But before I migrate my data, I will look a bit deeper.