Should I buy an Annuity? Good question. Annuities are complex financial products. In this post, we’ll try and explain what an annuity is, some of the variations, and why an investor may want to consider one.

An Annuity is an Insurance Product

An annuity is an insurance product. Much of what we talk about on finance-abcs.com is related to investments and investment products that are sold by banks, brokerages, or even governments (treasury bonds). Annuities are different in that they are a contract between the policyholder (us) and the underwriter (insurance company). This is important because in addition to being an investment product, an annuity is an insurance product which has some form of a guarantee that is backed by the insurance company.

Annuity Brokers and Salespeople

Aside from ourselves, who we’ll refer to as the policyholder, and the insurance company who writes the policy and provides the guarantee, there is often a 3rd party in the middle. While you can buy an annuity contract directly from an insurance company, you may buy one through a broker, financial advisor or other investment professional. It’s important to know the role of all parties involved. We’ll discuss why in a bit.

Annuity Types

To prepare for this post, I did some reading. I think I know less about annuities now. Fixed Annuities, Variable Annuities, Fixed Indexed Annuities, Deferred Annuities, Immediate Annuities…pretty confusing. Let’s leave all this aside for now and take a big step back.

Annuities Provide a Guarantee

It can be overwhelming to be responsible for managing our money in retirement. In the good old days of defined benefit pension plans (read more here), we worked for a company for our entire career, and when we retired, we got a paycheck every month until we died. Pretty simple.

Fast forward to today and defined contribution plans are the new standard. Each of us is responsible for saving for retirement. And then when retirement comes, we need to manage that nest egg, deciding what to invest in, how much to allocate to stocks, bonds, and cash (see more on asset allocation here), and how much we can take out each month to live on.

That’s a lot of work and uncertainty. Wouldn’t it be great to have some guarantees? That’s exactly what an annuity provides.

Annuity Options are almost unlimited

There are lots of types of annuities as well as individual features that can be added to each type that make the annuity landscape complex. We’ll touch on the basics so that we’re able to have an informed discussion, but if an annuity seems attractive to you, find an insurance company representative or advisor that you trust, and dig in to the details.

Guaranteed Income

I’m not sure this is a term that annuity professionals use, but it is a term that helps me think about this type of annuity. Guaranteed income annuities provide the purchaser a guaranteed income stream for a specified period of time. Typically, the purchaser makes a lump sum payment to the insurer in exchange for a monthly benefit payment. The benefit payment will vary based on the age, life expectancy, lump sum amount, and features chosen at the time the annuity is purchased.

We’ll look at an example in a bit, but this type of annuity is for someone who has saved for retirement and wants to convert their retirement savings into a dependable income stream so that they don’t need to worry about choosing investments or risking a market downturn.

To me, this type of annuity is similar to our old friend the defined benefit plan.

Guaranteed Rate

Another likely made-up term. In a guaranteed rate or guaranteed minimum return annuity, there is no promise of an income stream. Instead the insurer will guarantee that the purchaser will receive a minimum return on their investment each year. Often times, the insurer guarantees the principal investment and promises a variable rate of return. Depending on the annuity type, the purchaser may have more or less control in choosing the investments. We’ll look at some variations later.

Guaranteed rate annuities are more like the defined contribution plan in that the annuity purchaser has more control over the investing, and specific payment amounts are not guaranteed.

We’re Paying for a guarantee

We’ve used the word guarantee quite a bit. There is a reason for this. Any annuity we buy is an insurance contract. Most of what we discuss at finance-abcs.com are investments: stocks, bonds, mutual funds, ETFs… For all these investments there are no guarantees.

An annuity on the other hand is an insurance product that comes with a guarantee. That’s what we’re paying for. We buy an annuity because we want some certainty. Either certainty that we will receive a check in the mail every month for a specified period, or the certainty that we will not lose money in the market, ever.

Guarantees Aren’t Free

The insurance company is taking on risk. If we choose an annuity that gives us a payment stream for life, the insurance company is taking the risk that we could live until we are 108 years old and they’ll have to continue paying well beyond the average life expectancy. If we choose an annuity that guarantees our principal and a 4% per year gain, the insurance company is taking the risk that the market may underperform and they will still need to make good on their promise.

The insurance company charges annuity purchasers a fee to take on that risk. The fee may be imbedded in the policy assumptions, or it may be explicitly stated (like an expense ratio) in the annuity investment choices. More on fees later, but be aware that you are paying for guarantees.

Also, don’t feel bad for the insurance companies. They have actuaries who work with tons of data on life expectancy and investment returns that enable them to make good decisions on how to offer a product that provides guarantees for policy holders and is profitable for the insurer. Everybody wins.

Immediate Annuity

An immediate annuity is an example of the guaranteed income annuity. When buying an immediate annuity, the purchaser is trading dollars today for income in the future. The issuer, who is typically an insurance company, takes the purchaser’s payment and invests it. The insurance company is betting that it can grow the purchaser’s money at a higher rate than the rate it is paying.

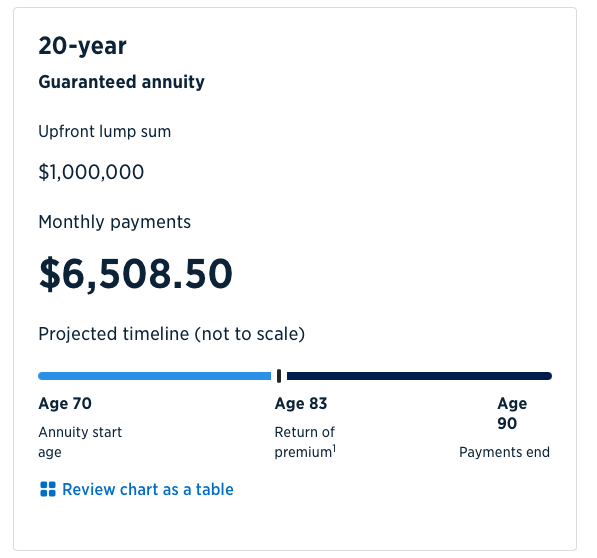

Let’s look at an example. I used USAA’s online annuity quote here. This is for demonstration purposes so that we can talk about how annuities work.

Here’s the scenario. Ellie Fant has saved well over a long career and has $1,000,000 in her 401k – great work Ellie!

She’s happy about where she is now financially, but worried about the future. She’s concerned about interest rates, the stock market, international instability, and she’s not confident that she can manage her $1,000,000 in a way that it will last for 20 years of retirement.

Ellie decides she needs the stability of fixed monthly payments. She plans to take the whole $1,000,000 and purchase an annuity. Ellie is 70 years old now and she plan to purchase a 20 year immediate annuity.

How An Immediate Annuity Works

Ellie sends a $1,000,000 check in to the insurance company. She signs a contract that says for her $1,000,000, she will receive a check for $6,508.50 every month for the next 20 years.

Over the course of the 20 years, Ellie will receive a total of $1,562,040 in payments. Not bad considering she only gave them $1,000,000. Also, this is guaranteed, unlike any investments Ellie could have made in bonds, stocks, or mutual funds.

Ellie traded a million dollars for the certainty of regular monthly payments.

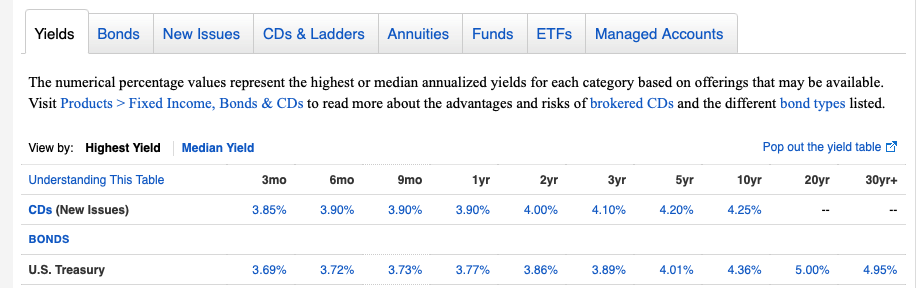

How does an immediate annuity compare to a Treasury Bond?

We’ve traded our $1,000,000 for a guaranteed monthly payment for the next 20 years. Let’s look at what might have happened if we took the money and invested in a 20 year treasury bond instead.

Fidelity tells me that today, I can get 5% return on a 20 year treasury.

So if Ellie bought a 20 year treasury, she would not have a guarantee, but she’d have a bond backed by the full faith and credit of the US Government. In the financial world, this is as close to a guarantee as we can get.

At 5% annually, Ellie’s million dollar bond will pay her $50,000 per year. That comes to $4,166 per month.

That’s over $2,000 per month less than the annuity. Can Ellie live on $2,000 less? Does she want to?

But at the end of the 20 year annuity period, Ellie has nothing. She traded her million for the guaranteed income.

At the end of the 20 year bond period, Ellie gets her $1 million back. That’s something to consider.

Immediate Annuity Considerations

Can we live on $50,000 annually v. the $78,096 that we’ll get with the annuity? Can we manage a semi-annual treasury bond payment v. a monthly check? And the big question is whether we’re OK with getting nothing back after 20 years of Annuity payments. What if I live longer?

The trade-off is the guaranteed $6,508 per month for 20 years v. the lower annual payment and the uncertainty. Annuity buyers are looking for certainty, and that certainty comes at a price.

Inflation will eat into our payments

This is an important consideration, so it get’s it’s own section. That $78,000 per year sounds pretty good. I’ve got a budget and I can see that this will cover my expenses with some left over for traveling and golf. Awesome!

Just remember, that $78,000 per year is fixed for the 20 year contract. Will $78,000 cover all of our expenses in 2046? It may, it may not.

Here’s the problem. That $6,508 per month doesn’t change. Not in year 5, not in year 10, not in year 20. That’s the guarantee.

Assuming a fairly modest 2.5% annual inflation rate, that $78,000 will have the purchasing power of roughly $47,000 in today’s dollars by 2046. Groceries, utilities, healthcare — they’ll all cost more. Our annuity paycheck won’t keep up.

This is why some annuity contracts offer an inflation adjustment — typically a 2–3% annual increase in your payment. It sounds great, but it comes at a cost: your starting payment will be lower. You’ll need to decide whether the peace of mind of keeping up with inflation is worth the smaller check in the early years.

There’s no right answer. But if you’re buying an annuity that will last 20+ years, we’d better have a plan for inflation.

Deferred Annuity

A deferred annuity is similar to the immediate annuity. The main difference is that while we sign the contract and start paying today, we don’t plan to receive payments until some point in the future. Since the insurance company is getting money today that it will not need to payout until a time in the future, it has a longer investment period and will likely offer a larger benefit (payment amount or additional features).

Fixed, Variable, Indexed Annuities

This group of annuities generally provide a guaranteed rate of return instead of a guaranteed payment (like the immediate or deferred annuity). As you might expect, fixed annuities provide a fixed rate of return for the life of the contract. Variable annuities provide a variable rate of return. Indexed annuities typically provide a rate of return that is linked to a particular market index like the S&P 500.

The level of guarantee provided, v. discretion of the policy-holder can be pretty broad.

High Discretion / Low Cost

I have a product called a retirement annuity that provides no guarantees, but allows me to invest money in a tax-deferred vehicle. I have total discretion in choosing amongst the equity, fixed income and money market investments that the contract offers. There is no guarantee that the investments will not lose value, and there is no guarantee that I will achieve a minimum rate of return. All I get from this is the ability to invest after tax money and not pay taxes on gains until I make a withdrawal.

Not much of a guarantee, but there is no up-front cost. The mutual-fund-like investments that the contract offers charge a minimal expense, which is what I pay for the ability to defer taxes.

Low Discretion / Higher Cost

I attended a sales seminar on indexed annuities. I really liked the advisor who was selling the product and I even considered investing. Here’s the pitch:

- Aside from a few relatively small pull-backs, the stock market (S&P 500) has been uncharacteristically strong since 2009.

- Wouldn’t it be great to take your gains now and lock in a guaranteed rate of return for the foreseeable future?

Yes

Of course it would.

This particular annuity guarantees that we will not lose our principal investment. It also guarantees a rate of return between 0 and 7% (I think these were the numbers) each year. If the S&P 500 returns 0 or is negative, our return is 0. If the S&P 500 is positive, we receive a portion of the S&P 500 gain, up to a maximum annual gain of 7%.

This seems like a pretty good deal. I’ll never lose money and the trade-off is that when the market is up big, my max return is 7%.

There were also some cash bonuses (paid to the policyholder) involved, which I didn’t completely understand, but it certainly was a compelling sales pitch for protecting money in retirement.

More Annuity Extras, Risks and Protections

The annuity industry is quite complex. There are many variations of the guaranteed rate type of annuity that can give investors some ability to choose investment options or adjust asset allocation. There are some that offer benefits like life insurance, or spousal benefits. Be sure to understand the benefits, responsibilities, as well as what you’re paying for. It’s important to have an insurance agent or advisor that you trust to help navigate.

Advisors

Whether it’s an advisor who works for the insurance company that is selling the contract, or an independent advisor, there is likely someone who will work with you to establish an annuity. This person is getting paid. Be sure you know how. You may want to meet with a few advisors before deciding who to deal with. This is a complicated space. Be sure you are working with someone you trust.

Risk

The guarantee, whether it is regular payments or a fixed rate of interest, comes from the insurance company that sells the annuity. What happens if the insurance company goes bankrupt? While I couldn’t find any evidence of this happening in the last 10 years or so, it’s pretty likely that the next 20 years or so will see some sort of financial crisis like we saw in 2008, 2001, etc… We’ve got our retirement riding on this annuity. We want to be certain that we’re protected.

Protections

Most insurance companies manage their policies quite conservatively. They are not betting our annuity money on bitcoin, they are more likely putting it in treasuries. But, we still want to be sure we’re protected. Insurance companies are rated by independent agencies like AM Best, Fitch and Moody’s. These agencies provide a financial strength rating that we, as potential customers can use to assess the likelihood that our annuity provider can keep their commitments.

Many insurance companies will reinsure pieces of their business. They essentially buy insurance policies with other insurance companies to reduce their risks.

Finally, most states provide some sort of protection for policy-holders. The federal government does not, so the rules are different state by state. Be sure to understand how your state deals with insurance company failures.

Before choosing an annuity, be sure to assess the financial strength of the insurance company that writes the annuity (note, this may not be the firm that sells you the annuity). And be sure to understand the other protections the insurance company and your state provide.

That’s a lot…This is why you need to buy your annuity contract from an advisor that you trust.

Is An annuity right for me?

That’s a really complicated question. If I’m concerned about managing my money in retirement, and some sort of guarantee is appealing to me, then yes, I should probably consider an annuity.

That’s the easy part. Now I need to decide what type of a guarantee I want and how much discretion I may want to have in my investment choices within the annuity. Some may say none, just send me a check. Others may feel like they want to be able to adjust their asset allocation to meet some of their goals in retirement.

The good news is that there are lots of options in the annuity market to satisfy most needs.

This is why finding a trusted annuity advisor is key. This person can help you navigate the options and features to develop a custom product that’s right for you.

Who Should (and Shouldn’t) Buy an Annuity

So should you buy one? Let me try and make this simple.

An annuity might make a lot of sense if:

- You’re retired or close to it, and the idea of managing your own investments stresses you out

- You don’t have a pension, and you want something that feels like one

- You have more money saved than you’ll realistically need, and you want to protect a chunk of it

- You’re worried about outliving your money — and honestly, that’s a very reasonable thing to worry about

An annuity probably doesn’t make sense if:

- You’re young and still in the accumulation phase. Time and compounding are on your side. You don’t need guarantees yet.

- You need flexibility. Annuities are not liquid. If you lock up your savings and then need the money for a medical emergency or a leaky roof, you may face steep surrender charges to get it back.

- You’re already well covered. If you have Social Security, a pension, and enough in savings to cover your expenses several times over, the guarantee an annuity provides may not be worth the cost.

- You like managing your own money and you’re good at it. If you’re a disciplined investor and market swings don’t rattle you, an annuity probably isn’t adding much.

There’s no universal right answer here. It depends on your situation, your personality, and how you’d feel getting that guaranteed check every month versus watching your portfolio go up and down.

What Are You Actually Paying? (Fees Explained)

Let’s talk about fees, because this is where annuities can get ugly.

Here’s the thing: you’re always paying for a guarantee. The question is how much, and whether you know it.

With a fixed or immediate annuity, fees are often baked into the payout rate. The insurance company offers you $6,000 a month instead of $6,500. That difference is their margin. You may never see a fee line item, but you’re paying.

With variable annuities, the fees are more explicit — and more expensive. Here’s what you might see:

- Mortality & Expense (M&E) fee: Typically 1–1.5% per year. This is the insurance company’s charge for providing the guarantee.

- Administrative fees: Usually small, maybe 0.10–0.25% per year.

- Subaccount (investment) fees: The mutual funds inside a variable annuity charge their own expense ratios. These can be another 0.5–1.5% on top of everything else.

- Rider fees: If you add features — like a guaranteed income rider or a death benefit rider — each one costs extra. Often 0.5–1% per year each.

Add it all up and a fully-loaded variable annuity can cost you 3% or more per year. Compare that to a low-cost index fund at 0.03% and you can see why some financial advisors are not fans.

None of this means annuities are a bad deal. It means the guarantee has a price. Know what you’re paying before you sign anything.

State Protections — The Safety Net You Hope You Never Need

I mentioned that insurance companies can go bankrupt. It’s rare, but it happens.

Here’s the good news: most states have a guaranty association that provides a backstop for annuity policyholders if their insurance company fails. Think of it like FDIC insurance for annuities, except it’s run at the state level.

The coverage limits vary by state, but a common level is $250,000 in annuity benefits. If you’re putting $1,000,000 into an annuity with a single insurer, that’s something to think about. Some buyers spread their money across multiple companies to stay within the guarantee limits at each one.

You can find your state’s specific coverage at nolhga.com (National Organization of Life & Health Insurance Guaranty Associations). Not exactly a household name, but worth knowing about.

Beyond the guaranty association, most reputable insurance companies manage their policy obligations very conservatively — we’re talking treasuries and high-grade bonds, not crypto. And many reinsure portions of their business with other insurers to spread their own risk.

Still, before you hand over a significant chunk of your retirement savings, check the insurer’s financial strength rating with AM Best, Fitch, or Moody’s. You’re looking for an A rating or better. This information is publicly available and your advisor should be able to point you to it.

Questions to Ask Before You Buy

Whether you’re talking to an insurance company rep or an independent advisor, here are the questions I’d want answered before I signed anything.

About the advisor:

- How are you compensated on this product? Is it a commission, and if so, how much?

- Do you represent multiple insurance companies, or just one?

About the annuity:

- What is the surrender charge period, and what happens if I need my money early?

- What are all the fees — M&E, admin, riders, subaccounts — and what is the total annual cost?

- Is there an inflation adjustment option, and what does it cost?

- What happens to my money when I die? Does it go to my heirs, or does the insurance company keep it?

About the insurance company:

- What is this company’s AM Best rating? (Look for A or better)

- Is this policy covered by my state’s guaranty association, and up to what amount?

If an advisor pushes back on any of these questions, or can’t answer them clearly, that tells you something important.

People Also Ask

What is the downside of an annuity? The main downsides are cost, complexity, and lack of flexibility. Annuities — especially variable and indexed annuities — can carry high fees that eat into your returns. They also typically have surrender charge periods of 5–10 years, meaning you’ll pay a penalty if you need your money early. And unlike a brokerage account, you can’t just change your mind and sell.

How much does a $100,000 annuity pay per month? It depends on your age, the type of annuity, and current interest rates. As a rough example, a 70-year-old purchasing a $100,000 immediate annuity today might receive somewhere in the range of $600–$700 per month for life. Younger buyers will receive less, since the insurance company expects to pay out longer.

Is an annuity better than a 401(k)? They’re different tools for different purposes. A 401(k) is a tax-advantaged savings vehicle — you’re building a nest egg. An annuity is typically something you buy with money you’ve already saved, to convert it into a reliable income stream. Many retirees use both: a 401(k) to accumulate, and an annuity to create guaranteed income in retirement.

Are annuities safe? The guarantee behind an annuity is only as good as the insurance company providing it. That said, insurance companies are heavily regulated, most manage their obligations conservatively, and most states provide guaranty association protection up to certain limits. Stick with highly-rated insurers (AM Best A or better) and you’re unlikely to have a problem — but no investment is completely risk-free.

Can you lose money in an annuity? It depends on the type. Fixed and immediate annuities protect your principal. Indexed annuities typically protect your principal but cap your upside. Variable annuities, where your money is invested in market subaccounts, can lose value if those investments perform poorly. Read the contract carefully and understand exactly what’s guaranteed and what isn’t.

Brian’s Take (Bottom Line)

I’ll be honest with you — I don’t own an annuity. I attended that indexed annuity sales seminar a few years ago and I found it compelling. I also decided it wasn’t right for me at the time.

I like managing my own money. I’m comfortable with market risk. And I have enough flexibility in my budget that a market downturn isn’t going to upend my retirement.

But I get why annuities appeal to people. The guaranteed paycheck is a powerful thing. If the market dropped 40% tomorrow and you knew your $6,400 was still showing up on the first of the month — that’s worth something real.

If you’re someone who loses sleep over the market, if you don’t have a pension and you’re scared of outliving your savings, an annuity might be exactly what you need. Not because it’s the highest-return option. But because sleep is underrated.

Just go in with your eyes open. Understand what you’re paying. Ask hard questions. And work with someone you trust — not someone who’s just trying to close a sale.