Get Started Investing

We’ll talk a little about why we want to invest and how to select investments, but once we’re thinking about investing, act like Nike and “just do it“. Now, this does not mean that we should take our life savings and put it into the hot stock tip that our Uncle Fred shared at the last Christmas party.

I’m talking about opening a brokerage account (it’s free to open), transferring a few dollars in from our checking account (also free), and buying a stock or a mutual fund.

I can take $5 and buy a fractional share of almost any publicly traded company or any mutual fund.

Publicly Traded Company

What’s that?

Simply put, a publicly traded company is a company whose ownership shares trade on a registered exchange like the New York Stock Exchange (NYSE) or the National Association of Securities Dealers Automated Quotes (NASDAQ for short).

Companies are generally started in someone’s garage. Someone has a great idea, and just gets started. If it works out, the company grows. As it gets bigger, the company finds itself in the position where it needs to raise capital (money) to buy office space, hire employees, advertise… One of the ways a company can do this is by going public. This simply means that the owner or owners sell some shares to outsiders and these shares then start trading on an exchange and can be bought and sold by the public. Read the post on capital markets if your interested in how this works, Click here.

Some companies choose to remain private. Once a company sells shares to the public, those shareholders have a say on how the company runs. To retain control, some companies look for other funding sources like loans or private investors.

Chik-fil-A is an example of a private company. We can buy a sandwich and waffle fries, but not shares of the company. McDonalds is a public company. We can get a Big Mac and buy shares of the company.

Mutual Fund

A mutual fund and an Exchange Traded Fund (ETF) are very similar. they are both baskets of securities. I’ll use the term mutual fund to refer to both. More about funds and ETFs here.

A mutual fund is a great investment choice. There are thousands of mutual funds to choose from, all of which are baskets of securities. This means that the fund buys shares of publicly traded companies, or bonds, or both. The mutual fund owns lots of securities so we get the benefits of investing without the responsibility of picking winners. A fund manager or an index does this. Read more about mutual funds here and here.

Fractional Shares

In the old, old days, if I wanted to invest in a publicly traded company, I had to buy round lots of 100 shares. I couldn’t buy just one because the buying process was manual. I called my broker and requested the buy, he called down to the exchange where a trader had to yell and scream the order to get a seller’s attention.

It was also expensive. I might pay hundreds of dollars in commissions to the brokers involved. This made it impractical to trade only a few shares.

Today, all of this is automated. I type an order into my computer, it shoots off to the exchange, one computer talks to another, buyers are matched with sellers and trades happen in the blink of an eye.

Up until recently, stock trades cost about 5 bucks. Robinhood (the trading platform not the fictional bandit) introduced free trades and all the kids followed along. Most stock trades are now free. Yay.

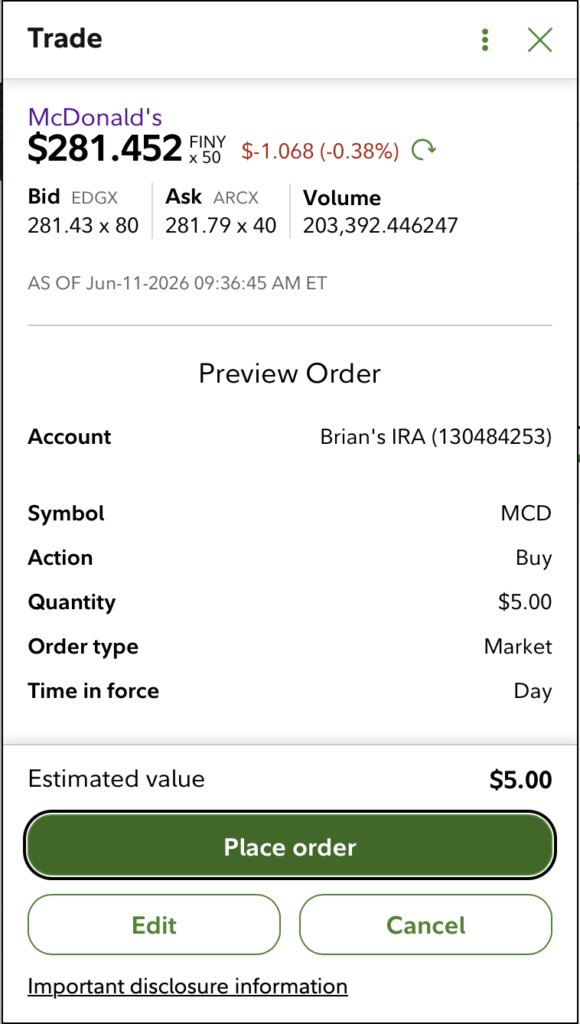

And I can buy a small piece of a share. I don’t have to buy a whole share. I’d love to buy some McDonalds stock, but I only have 5 bucks and a share costs over $200.

In the old days, I’d be out of luck. Not today.

I’ll only get 5 / 281.452 = 0.0177 shares, but I’m a shareholder. Read more about stock ownership here.

Get Started

My point here is that the best way to learn is to get started. Open a free brokerage account. I recommend using one of the big 3 – Fidelity, Vanguard or Schwab. Here’s a post that talks about why and exactly how to open one.

But while a trading platform like Robinhood seems like a lot of fun, the big 3 offer tools, research, and education, that is far superior to what we’ll get on other platforms.

If you’re unsure what to buy, try a nice low-cost S&P 500 fund. Read here, here, and here for more about what the S&P 500 is and why you might want to invest.

Don’t let the thousands of choices overwhelm you. Take 5 bucks, open a free brokerage account, and invest it.

Congratulations!! You’re now an investor. Now take advantage of the educational material and research reports to start building a portfolio.

Choosing the best investment

As we’re now investors, it’s important for us to understand that choosing the best investment is impossible.

That’s OK.

As an investor, we’re going to build a portfolio – a group of investments that will help us achieve our goals.

Investing is a long game. Most of us start investing for retirement at our first job by participating in the company’s 401k plan. That’s a 40 year or more journey.

Many folks open up a 529 college savings plan for a child when they are young. Often they have 10, 15 or 18 years to save and invest before they’ll pay for college.

If our goal is to use investments to grow money to use next week or next year, we may be disappointed.

The S&P 500

The reason why investing is a long game can be demonstrated by taking a look at the S&P 500. The S&P 500 is a stock index (basically just a list of companies). In this case, it’s a list of the 500 largest publicly traded US companies. The S&P 500 is viewed as a proxy for the US economy and the US equity markets. That is to say that The S&P 500 represents what’s going on financially here in the US.

Over the past 100 years or so, the S&P 500 has returned about 10% per year with dividends reinvested. That means if we bought shares years ago, held them and reinvested our dividends (when a company or mutual fund pays a dividend, we can choose to either take the dividend in cash and spend it, or we can tell our broker to buy additional shares with the dividend), our investment would grow on average 10% per year.

On Average

Averages work by looking at a lot of data and taking, well, the average… In the case of the S&P 500, we’re taking the data since the early 1900’s and we’re saying on average, it returns 10% per year.

If we bought in 1940, we’d probably average about 10% per year, but there were some bad years and some good years in between. Here’s a picture of S&P 500 returns by year.

More up years than down. That’s good.

Some great years where it returned 40% or 50%. But some rough years too. In 2008 it was down almost 40%.

Context

Let’s say we have a nice windfall and we decide to invest $1,000 in an S&P 500 fund on January 2, 2008. At the 1/2/2008 price, we buy 0.69 shares. Let’s look at a picture.

The top header shows various dates. Row 1 shows the S&P 500 (Ticker ^GSPC) price on those dates. We see the $1,000 we invested and the 0.69 shares we got for that $1,000. Our value is $1,000 on the day of purchase. Subsequent columns tell the story of what happens as the S&P 500 price changes over the years.

Our value, after purchase is $1,000 as we’d expect.

Unfortunately, we bought right before the 2008 financial meltdown. By the end of 2008, the S&P 500 was down 37% and so was our investment.

We wisely invested our $1,000. But now we only have $623.24. 37% less than we started with. I don’t know about you, but this would make me panic. That’s real money.

The top row of the table shows the price of the S&P 500 (ticker symbol ^GSPC) on at the end of year on a few select years. It’s price has improved at the end of 2009, but we’re still down 11%.

But if we’re patient and keep our money invested, by the end of 2014, we have $1,420.64. That’s a 42.06% improvement from the $1,000 we started with. Great, but we’ve been invested for 7 years so that’s a 6.01% return, which is less than the 10% average annual return I told you about.

But, by the end of 2019, the S&P has gained 122.92% since that initial investment in January 2008. We’ve held on for 12 years and we’ve now achieved 10% average annual returns.

We invested at one of the worst possible times in history. We took it on the chin for the first 2 years, but then we slowly recovered and by 2019, we had achieved 10% average annual return.

What did we learn?

Investments are volatile. This means that they go up and down in value due to influences outside of our control. It’s not like our bank account that promises us a set interest rate and a guaranteed payment every year.

We’re taking a risk, and the over-sized return potential is the reward for taking that risk.

But, volatility means that our investments will lose value some years. Sometimes for several years in a row.

Don’t invest money you’ll need in the next 5 years.

Money we need for rent, groceries or our emergency fund should not be invested. It should be in a nice safe savings or checking account.

Read this post to see how time is critical to investment returns.

Choosing Investments

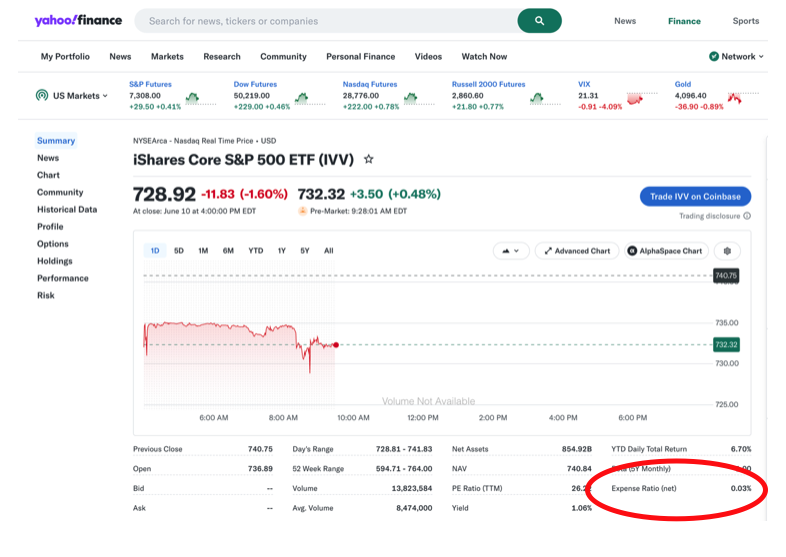

I like a nice low-cost S&P 500 fund like iShares Core S&P 500 ETF (IVV)

This fund tracks the S&P 500 index (^GSPC), meaning that it buys shares of all the companies in the index. The fund holds shares of the 500 largest publicly traded US companies. That means it owns McDonalds, Starbucks, Amazon, Apple, Walmart, ExxonMobil and 494 other companies.

And when I say low-cost, I’m referring to the expense ratio circled in red above on the yahoo stock quote.

An expense ratio of 0.03% means that the fund (IVV) will take $3 for every $10,000 we invest to pay fund expenses. That’s pretty cheap. We don’t write a check, it is automatically deducted from our returns. More about fund expenses here.

More about why I like the S&P 500 here.

But as much as I like this investment. As we’ve seen, it has down years. And some pretty big ones. Every stock, bond and fund I’ve owned has gone down in value at some point.

The Best Investment

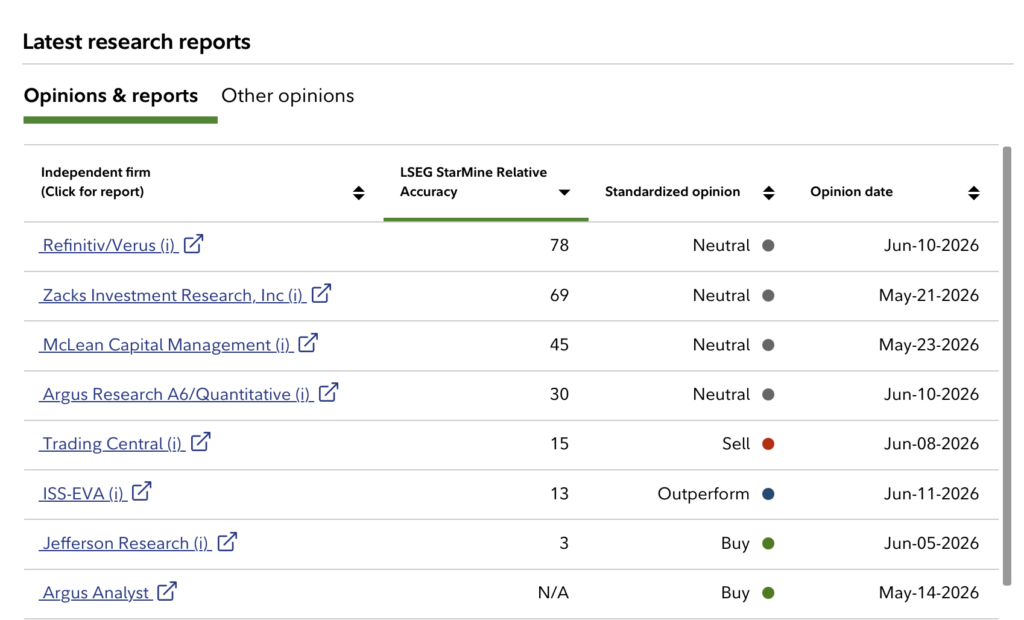

And as I mentioned, there is no best investment. Pick any company and there are really smart people that think that company is a buy (they’re optimistic or bullish), and there are others who think it’s a sell (they are pessimistic or bearish). Look at McDonalds.

The smart people (probably a bunch of Harvard MBAs who spend their entire day every day researching restaurant companies and the industry) at Jefferson Research think it’s a buy. While the Harvard MBAs doing the same thing at Trading Central think it’s a sell.

If these smart people don’t agree on what’s a good investment, what chance do we have?

A Thesis

Every investment requires a thesis. It could be a sentence or 2, but it’s about why we think this is a good place for our money. We worked hard for our money and even though we know it is impossible to pick the best investment, we need to pick a good one.

Diversify

And we need to diversify. We’ll make some mistakes. So we need to hold a portfolio of different types of investments. A mutual fund is a great way to diversify – look at an S&P 500 fund. It holds 500 companies in many different industries.

Asset Allocation

We need to spread our money across Cash investments, Fixed Income investments and Equity investments. Read more here. Equities like stocks have historically returned more than cash and fixed income, but they are more volatile. Cash is stable, however, we lose buying power to inflation and it is unlikely to grow at the pace we need. Fixed income typically provides lower growth than equity but a bit more stability.

Why Invest

This sounds like a lot of work. Why bother?

Well, unless we’re independently wealthy or we have a great pension (which few do these days) we need to save for retirement. I retired at 56 (had enough) and plan to live into my 90s (I hope). That means my investments need to generate the cash I’ll need to pay my expenses for 40 years with no paycheck.

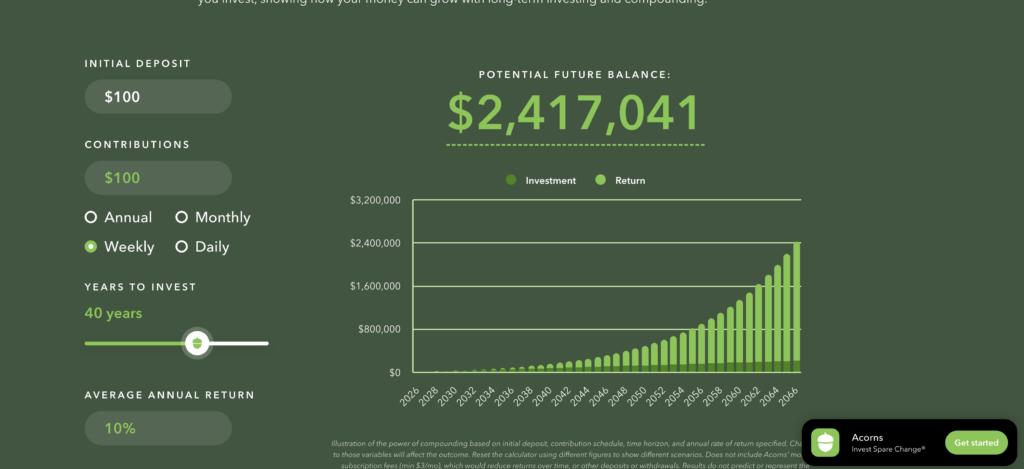

Here’s a comparison from the good folks at acorns.com.

I’m 20 years old so I’m investing for 40 years. I’m investing in a nice low-cost S&P 500 fund which we know has historically returned on average 10% per year with dividends invested over long periods. And 40 years is definitely a long period.

$100 out of my weekly paycheck could grow to over $2 million at retirement!!!

Or I could put it in a nice safe savings account earning 1%

$255,000 is nothing to sneeze at, but it’s not going to last me through my golden years. Trust me. I’m 6 years into retirement.

Go to acorns and try it out.

And read the post on compounding here.

Wrap Up

That’s a lot. A few key points:

- We need to invest. There is risk involved but without the magic of compounding, that investments provide, we’re unlikely to meet our financial goals.

- We should not invest money we need for groceries, rent or other near-term expenses. We need to find a way to put aside a few dollars from every paycheck and invest it.

- Start now! There are a million reasons not to start. It’s complicated, there are too many choices, I haven’t set aside enough money…Take 5 minutes and 5 bucks. Open a brokerage account at Fidelity, Vanguard or Schwab. And take the 5 bucks and buy fractional shares of a stock or mutual fund.

Here’s how to start: What’s a Brokerage Account and How Do I Get One?

Good luck!