Last year in the post That’s My Money… I wrote about the social security shortfall: how Social Security works, how it’s funded, and how it’s own trustees expect to run out of money. And about how we’re all angry because “that’s our money“.

As retirees, we’ve paid into social security via payroll taxes our whole working lives. Go to ssa.gov and create a free account and you can see exactly what you’ve paid into the program.

Is This Our Money?

This is a grey area. We paid payroll taxes to social security with a promise that we’ll get paid a benefit when we claim (as early as 62, or as late as 70, depending on whether we want the highest monthly payment amount or the earliest check.)

But social security is not like a 401k. In a 401k, we have our own account. I get statements or I can log in to see my balance. This money is mine. My ssa.gov account shows me a projected benefit but don’t confuse this with actual real money in an actual account with my name on it.

And in my opinion, the government and politicians have promised quite a few things they haven’t delivered upon, so I’m taking this all with a grain of salt.

So yes, we’ve paid taxes into a fund and we’ve been told an amount to expect, but it’s not really our money.

When Will Social Security Run Out?

In an article today, our good friend Clark Howard wrote that new projections show that social security could run out in 2032. Read it here.

“Run out”, likely means a reduction in payments of 22% according to the article.

And without action by congress, social security is likely to run out.

Congress?

I won’t rehash my thoughts in detail, but congress has the power to take action, but our overwhelming national debt which now sits at around $40 trillion severely limits our options.

So for the kids at home, this is why debt is a problem. With minimal debt, we have cash on hand or available credit to address pressing financial issues. With high debt and no cash on hand or easy credit, the only way to solve a financial problem is to take money from someplace else, or sit back and hope for the best.

So I wouldn’t put much faith in congress. They have a solid track record of avoiding the hard decisions and kicking the can down the road. How many times recently has the government shut down because congress couldn’t fund it??

So What Can We Do?

I took social security at 62.

All the articles I’ve read provide 2 choices. What happens if I take the smaller payment at 62, v. waiting til 70. At 62, we start getting paid earlier. At 70 we get a larger check.

From age 62 to about age 80, we’d be ahead taking payments early. But once we hit 80, we receive more money overall by waiting and taking the higher payment. And since most of us will live past 80, financial experts tell us to wait.

I came up with my own option 3. Take the payments at 62. Don’t spend them, invest them in a nice low-cost S&P 500 fund.

Growth

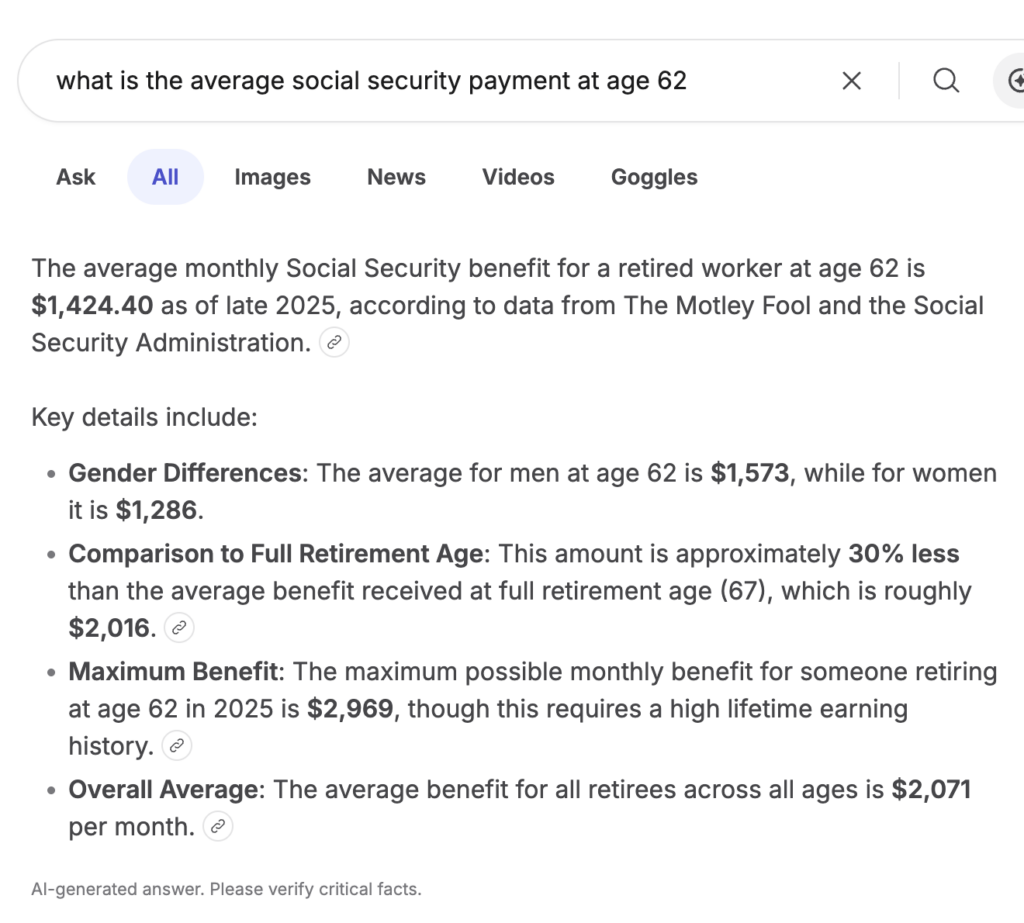

The average monthly social security payment at 62 is about $1,400. Let’s look at what happens if we take the payment at 62, invest every check in an S&P 500 fund returning an average 10% annual return.

I show up at age 70 with over $200,000 in my investment fund funded by my early (though lower) payments!!!

But My Monthly check is smaller

Yes. My monthly check if I waited until age 70 would be roughly $2,900. That’s a lot more per month. $1,500 per month more.

Those numbers are from AI so they have to be correct, right?

But my first point here is that I now have $200,000 saved. If I start spending my smaller $1,400 check at age 70, and I supplement it with $1,500 from my investment account (the $200,000), I will have $2,900 to spend each month for at least 11 years – til I’m 81.

But, I think it will be much more. I’m not taking the investment account and moving all $200,000 to cash at age 70. I’m leaving the bulk of it invested and drawing $1,500 per month. The rest continues to grow.

Risks

There is risk with this plan.

What if the S&P 500 tanks? What if we have years of lower than historic averages returns?

It could happen. So, yes, there is risk.

There is also risk that the crisis at social security worsens.

Risk is everywhere.

And Another Thing…

By taking social security at 62 and investing it, It is now in my pocket. It is my money.

If I have an emergency at 65, I can take money from my investment account. This could impact my ability to pay myself in future years, but that money is mine.

Try calling the folks at social security and asking for some cash at age 65.

Wrap Up

Social Security could make changes to improve it’s financial state. Congress could act to send more money to make up for the shortfall. Theoretically pigs could fly.

And congress or social security could make things worse. Gasp!

I’m betting on me. Give me the money now, let me invest it and I’ll take control.